6 Chapter 3 Lab

6.1 Autoregressive model (AR)

AR(p) process is correlation with lagged values of the data itself.

\[ X_t-\mu = \alpha \cdot (X_{t-1}-\mu)+Noise_t\]

Some simulation examples down below. Note how the coefficent \(\phi\) affects the look of the graph:

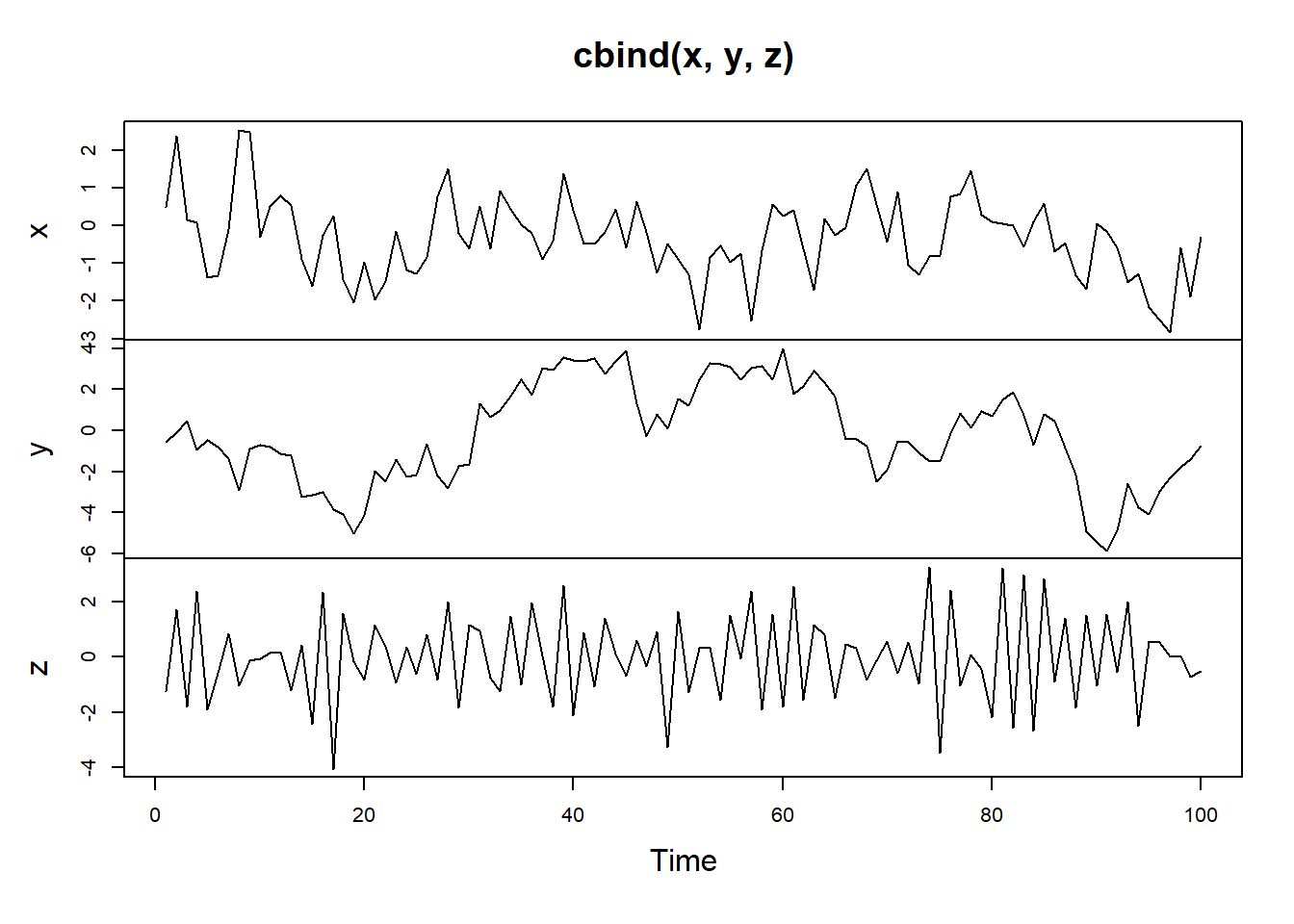

x <- arima.sim(model = list(ar = 0.5), n = 100)

# Simulate an AR model with 0.9 slope

y <- arima.sim(model = list(ar = 0.9), n = 100)

# Simulate an AR model with -0.75 slope

z <- arima.sim(model = list(ar = -0.75), n = 100)

plot.ts(cbind(x, y, z)) AR(1) model with slope \(\alpha=0.9\) creates a obvious trend while the negative slope creates a zic-zac pattern.

AR(1) model with slope \(\alpha=0.9\) creates a obvious trend while the negative slope creates a zic-zac pattern.

par(mfrow = c(3,1))

# Plot your simulated data

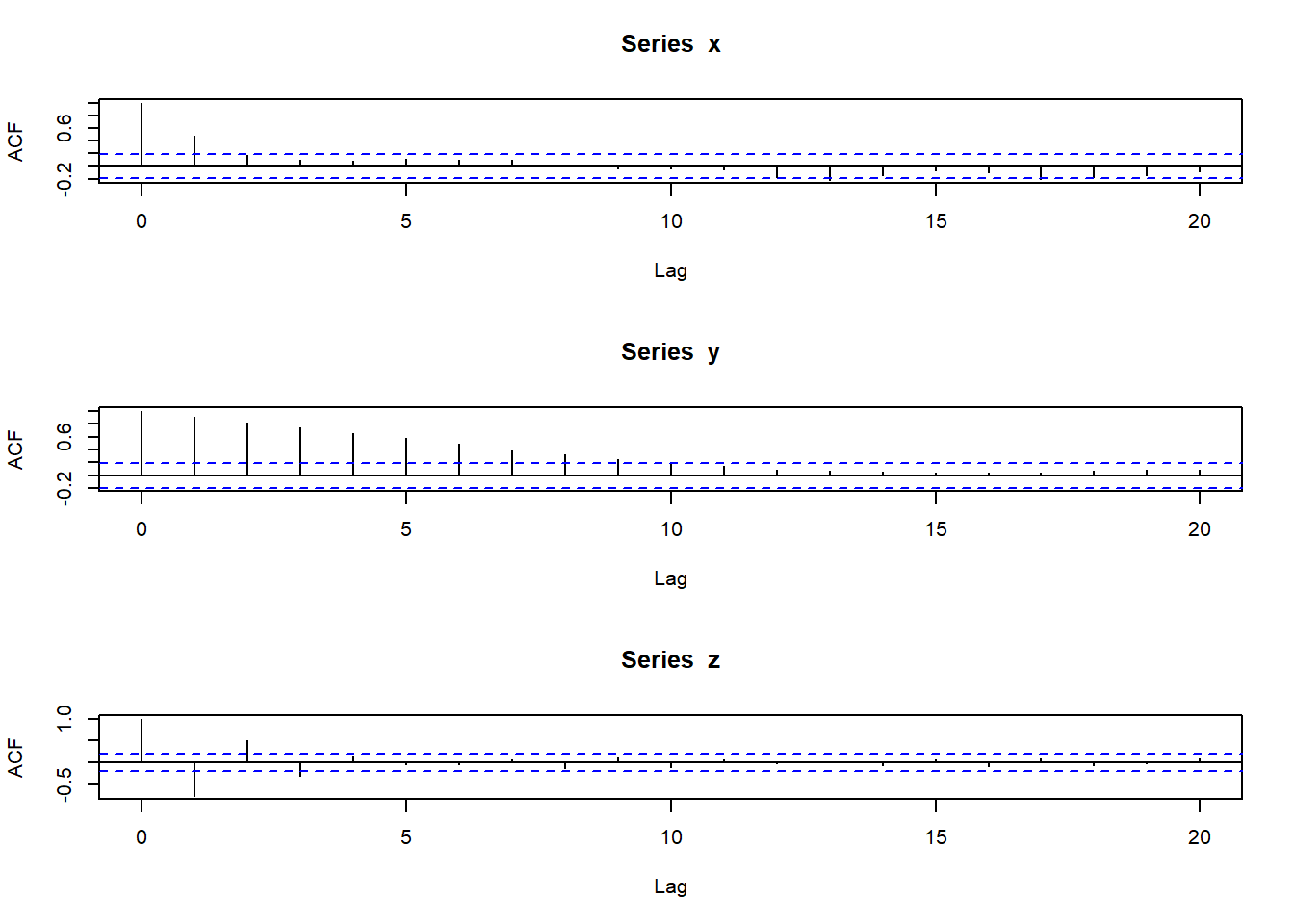

acf(x)

acf(y)

acf(z) The ACF plots tell a lot about each time plot:

The ACF plots tell a lot about each time plot:

Strong short-term positive correlation in early lags (1 and 2)

Strong short-term positive correlation in early lags up to lag of 5

Strong short-term negative correlation in early lags up to lag of 5

The PACF will tell us what AR(p) model would be appropriate for fitting this data

par(mfrow = c(3,1))

# Plot your simulated data

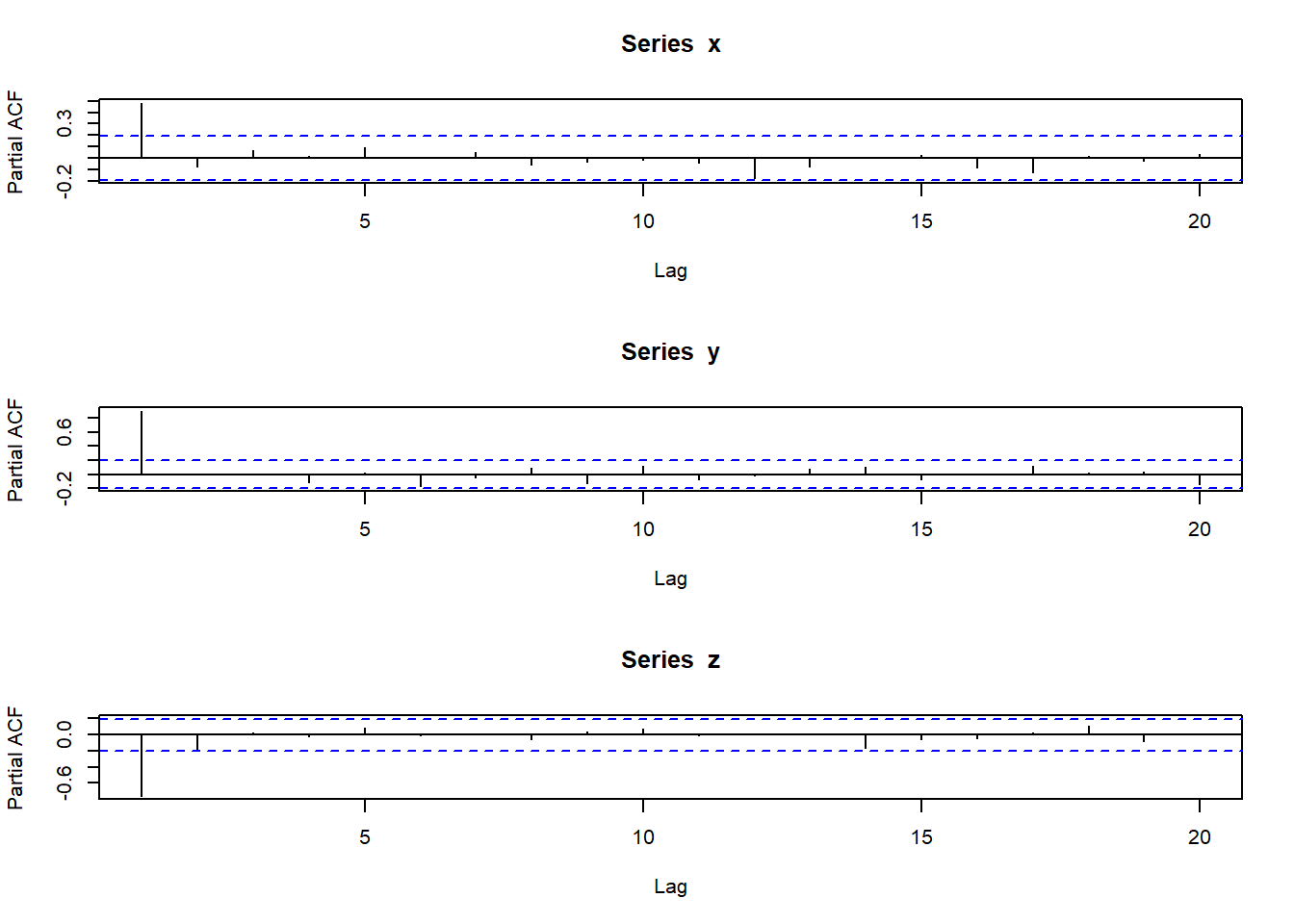

pacf(x)

pacf(y)

pacf(z)

The PACF plots tell us that a AR(1) model would be appropriate for all 3 data. This is expected since we used AR(1) models to generate these data.

6.2 Chicken Price

6.3 Chicken price

library(astsa)

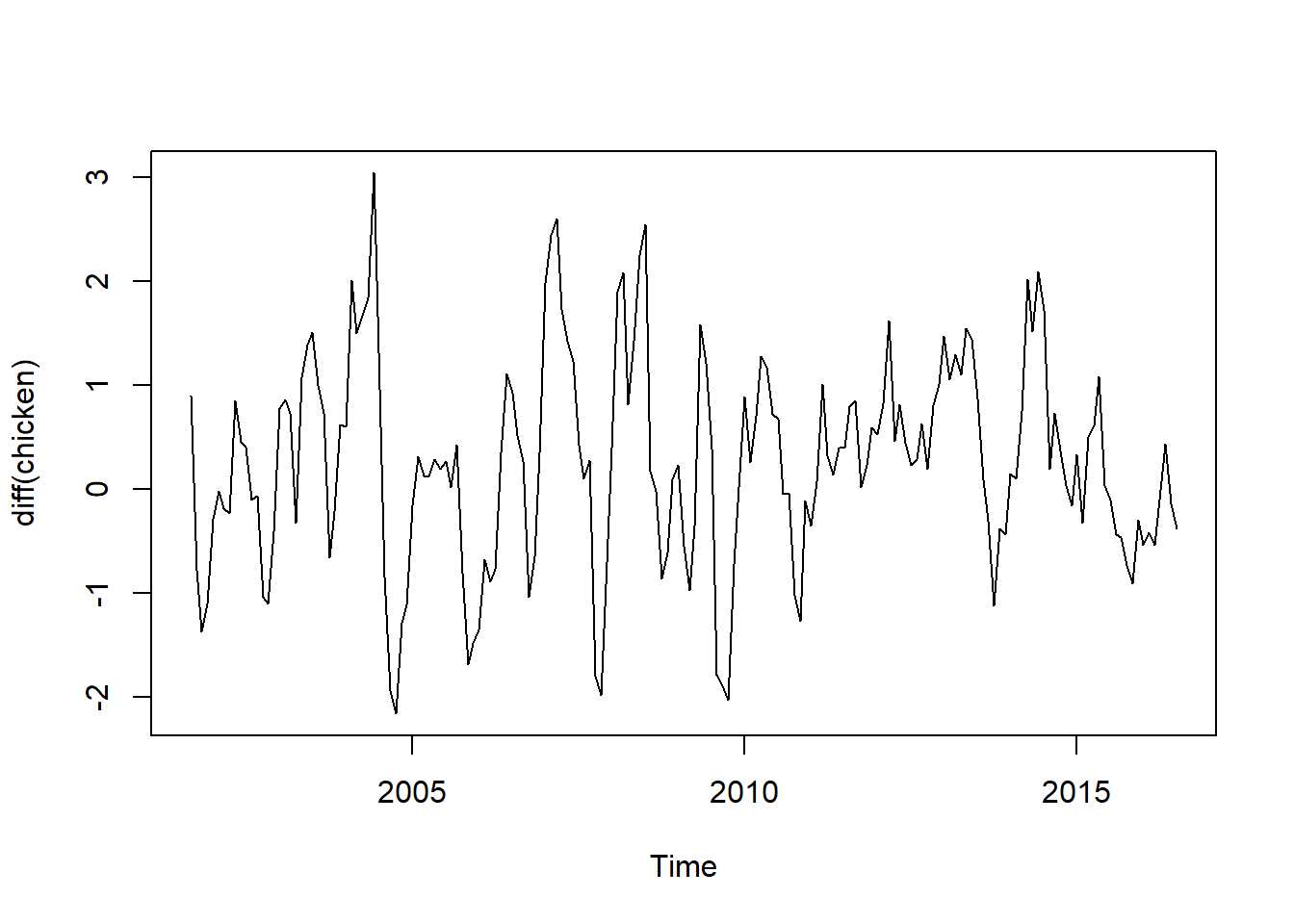

# Plot differenced chicken

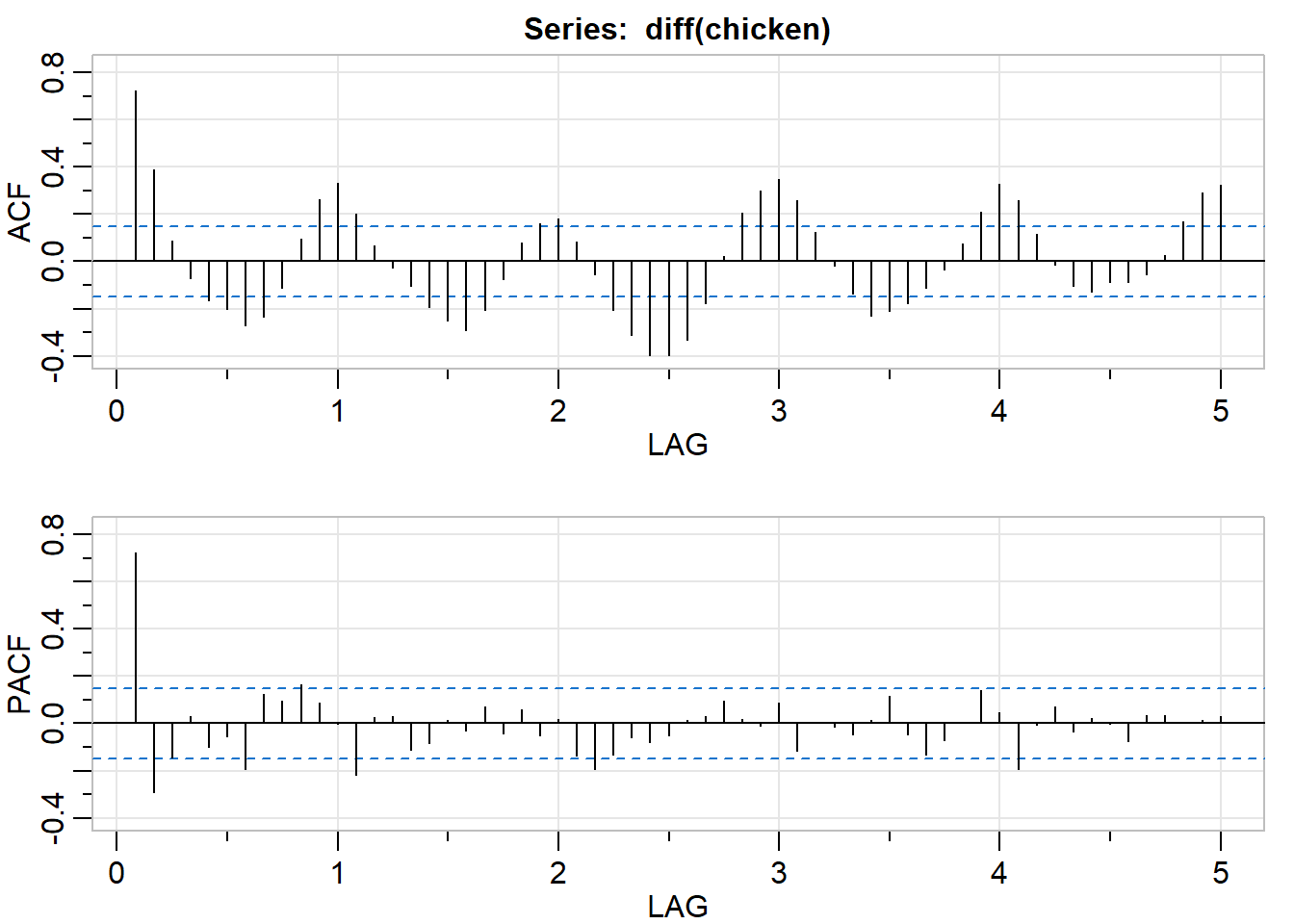

plot(diff(chicken))

# Plot P/ACF pair of differenced data to lag 60

acf2(diff(chicken), max.lag = 60)

## [,1] [,2] [,3] [,4] [,5] [,6] [,7] [,8] [,9] [,10] [,11] [,12]

## ACF 0.72 0.39 0.09 -0.07 -0.16 -0.20 -0.27 -0.23 -0.11 0.09 0.26 0.33

## PACF 0.72 -0.29 -0.14 0.03 -0.10 -0.06 -0.19 0.12 0.10 0.16 0.09 0.00

## [,13] [,14] [,15] [,16] [,17] [,18] [,19] [,20] [,21] [,22] [,23] [,24]

## ACF 0.20 0.07 -0.03 -0.10 -0.19 -0.25 -0.29 -0.20 -0.08 0.08 0.16 0.18

## PACF -0.22 0.03 0.03 -0.11 -0.09 0.01 -0.03 0.07 -0.04 0.06 -0.05 0.02

## [,25] [,26] [,27] [,28] [,29] [,30] [,31] [,32] [,33] [,34] [,35] [,36]

## ACF 0.08 -0.06 -0.21 -0.31 -0.40 -0.40 -0.33 -0.18 0.02 0.20 0.30 0.35

## PACF -0.14 -0.19 -0.13 -0.06 -0.08 -0.05 0.01 0.03 0.10 0.02 -0.01 0.09

## [,37] [,38] [,39] [,40] [,41] [,42] [,43] [,44] [,45] [,46] [,47] [,48]

## ACF 0.26 0.13 -0.02 -0.14 -0.23 -0.21 -0.18 -0.11 -0.03 0.08 0.21 0.33

## PACF -0.12 0.01 -0.01 -0.05 0.02 0.12 -0.05 -0.13 -0.07 0.01 0.14 0.05

## [,49] [,50] [,51] [,52] [,53] [,54] [,55] [,56] [,57] [,58] [,59] [,60]

## ACF 0.26 0.12 -0.01 -0.11 -0.13 -0.09 -0.09 -0.06 0.03 0.17 0.29 0.32

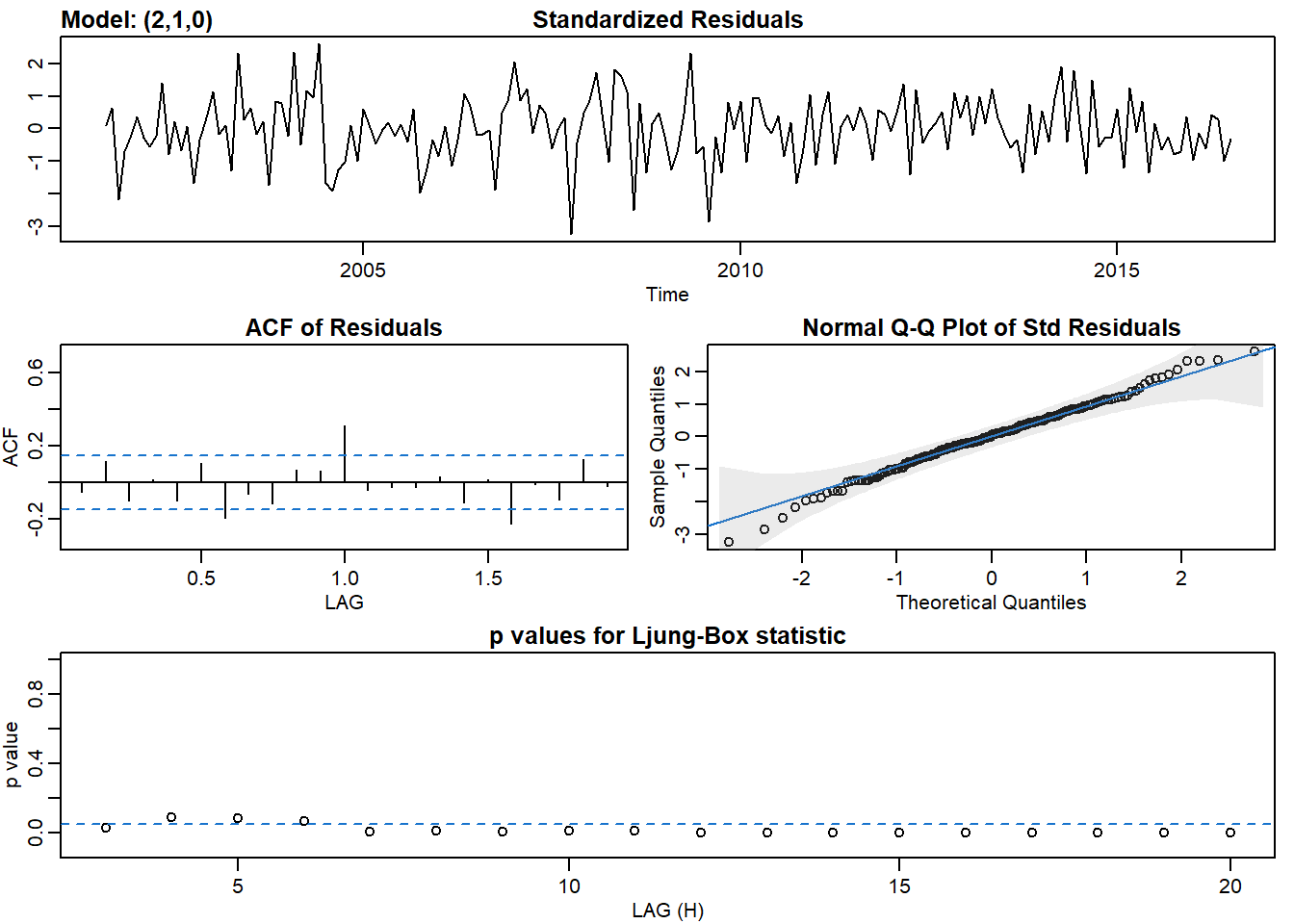

## PACF -0.20 -0.01 0.07 -0.04 0.02 0.00 -0.08 0.03 0.04 0.00 0.01 0.03# Fit ARIMA(2,1,0) to chicken - not so good

sarima(chicken, p = 2, d = 1, q = 0)## initial value 0.001863

## iter 2 value -0.156034

## iter 3 value -0.359181

## iter 4 value -0.424164

## iter 5 value -0.430212

## iter 6 value -0.432744

## iter 7 value -0.432747

## iter 8 value -0.432749

## iter 9 value -0.432749

## iter 10 value -0.432751

## iter 11 value -0.432752

## iter 12 value -0.432752

## iter 13 value -0.432752

## iter 13 value -0.432752

## iter 13 value -0.432752

## final value -0.432752

## converged

## initial value -0.420883

## iter 2 value -0.420934

## iter 3 value -0.420936

## iter 4 value -0.420937

## iter 5 value -0.420937

## iter 6 value -0.420937

## iter 6 value -0.420937

## iter 6 value -0.420937

## final value -0.420937

## converged

## $fit

##

## Call:

## stats::arima(x = xdata, order = c(p, d, q), seasonal = list(order = c(P, D,

## Q), period = S), xreg = constant, transform.pars = trans, fixed = fixed,

## optim.control = list(trace = trc, REPORT = 1, reltol = tol))

##

## Coefficients:

## ar1 ar2 constant

## 0.9494 -0.3069 0.2632

## s.e. 0.0717 0.0718 0.1362

##

## sigma^2 estimated as 0.4286: log likelihood = -178.64, aic = 365.28

##

## $degrees_of_freedom

## [1] 176

##

## $ttable

## Estimate SE t.value p.value

## ar1 0.9494 0.0717 13.2339 0.0000

## ar2 -0.3069 0.0718 -4.2723 0.0000

## constant 0.2632 0.1362 1.9328 0.0549

##

## $AIC

## [1] 2.040695

##

## $AICc

## [1] 2.041461

##

## $BIC

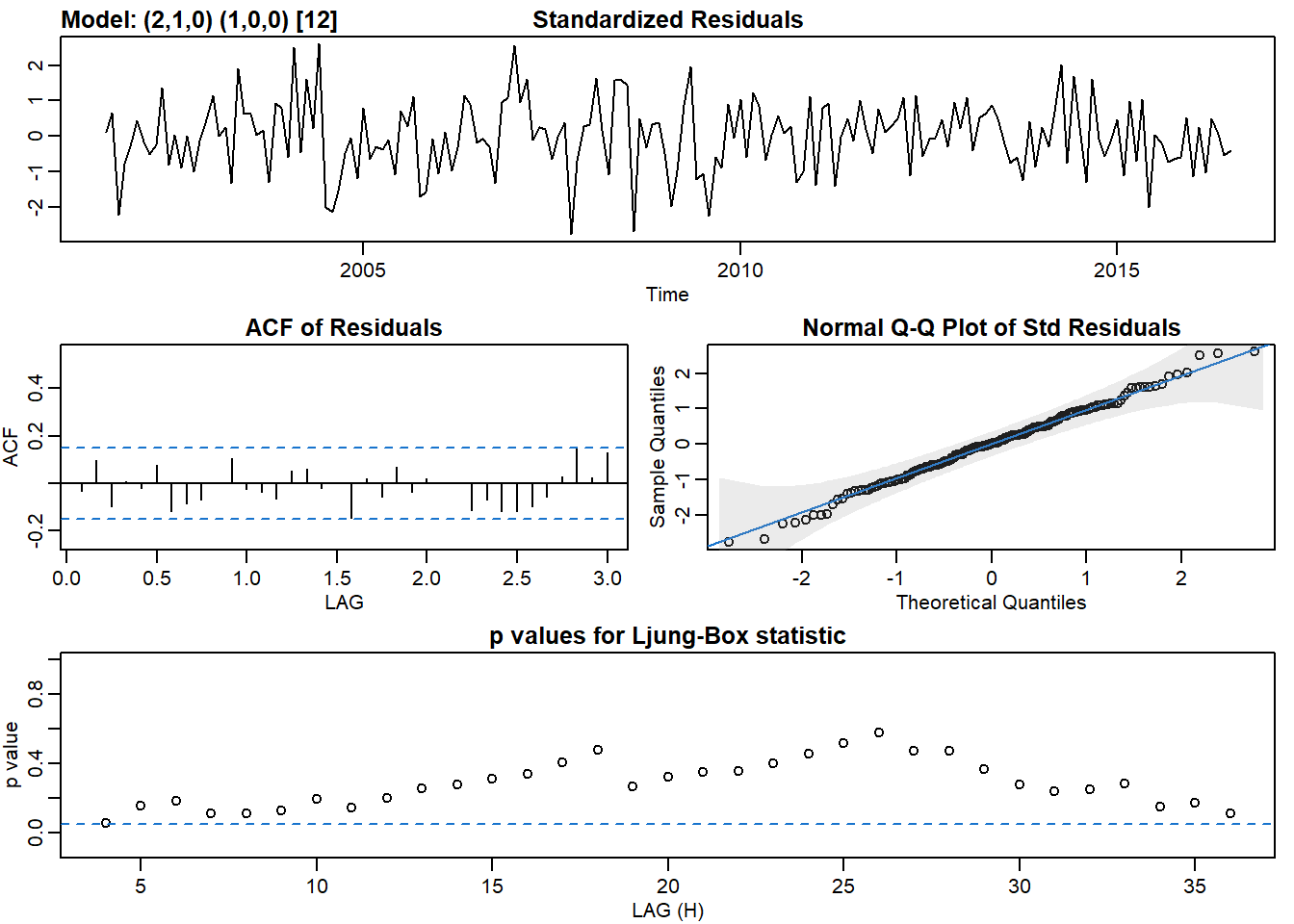

## [1] 2.111922# Fit SARIMA(2,1,0,1,0,0,12) to chicken - that works

sarima(chicken, p = 2, d = 1, q = 0, P = 1, D = 0, Q = 0, S = 12)## initial value 0.015039

## iter 2 value -0.226398

## iter 3 value -0.412955

## iter 4 value -0.460882

## iter 5 value -0.470787

## iter 6 value -0.471082

## iter 7 value -0.471088

## iter 8 value -0.471090

## iter 9 value -0.471092

## iter 10 value -0.471095

## iter 11 value -0.471095

## iter 12 value -0.471096

## iter 13 value -0.471096

## iter 14 value -0.471096

## iter 15 value -0.471097

## iter 16 value -0.471097

## iter 16 value -0.471097

## iter 16 value -0.471097

## final value -0.471097

## converged

## initial value -0.473585

## iter 2 value -0.473664

## iter 3 value -0.473721

## iter 4 value -0.473823

## iter 5 value -0.473871

## iter 6 value -0.473885

## iter 7 value -0.473886

## iter 8 value -0.473886

## iter 8 value -0.473886

## iter 8 value -0.473886

## final value -0.473886

## converged

## $fit

##

## Call:

## stats::arima(x = xdata, order = c(p, d, q), seasonal = list(order = c(P, D,

## Q), period = S), xreg = constant, transform.pars = trans, fixed = fixed,

## optim.control = list(trace = trc, REPORT = 1, reltol = tol))

##

## Coefficients:

## ar1 ar2 sar1 constant

## 0.9154 -0.2494 0.3237 0.2353

## s.e. 0.0733 0.0739 0.0715 0.1973

##

## sigma^2 estimated as 0.3828: log likelihood = -169.16, aic = 348.33

##

## $degrees_of_freedom

## [1] 175

##

## $ttable

## Estimate SE t.value p.value

## ar1 0.9154 0.0733 12.4955 0.0000

## ar2 -0.2494 0.0739 -3.3728 0.0009

## sar1 0.3237 0.0715 4.5238 0.0000

## constant 0.2353 0.1973 1.1923 0.2347

##

## $AIC

## [1] 1.945971

##

## $AICc

## [1] 1.947256

##

## $BIC

## [1] 2.0350056.4 Unemployment

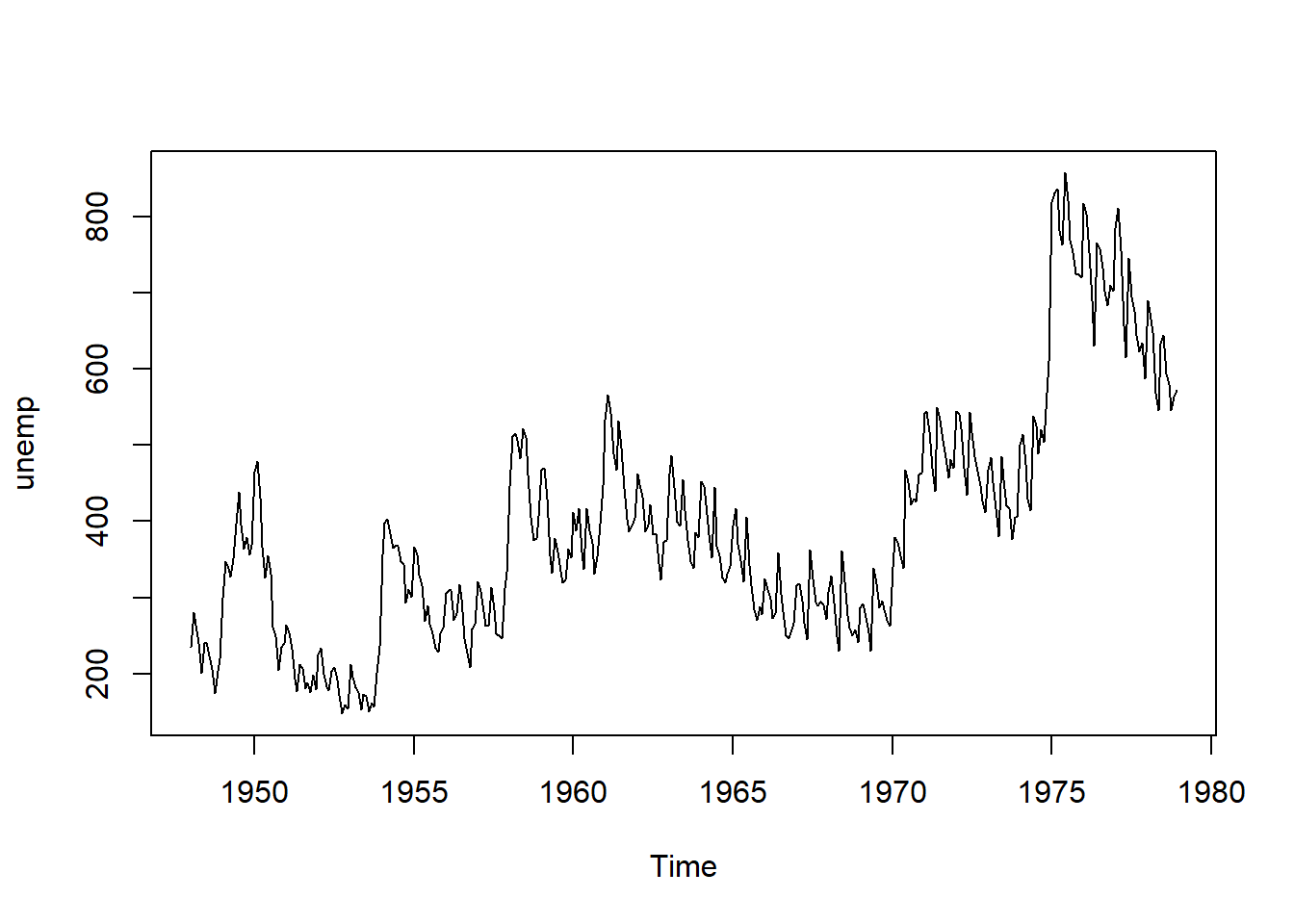

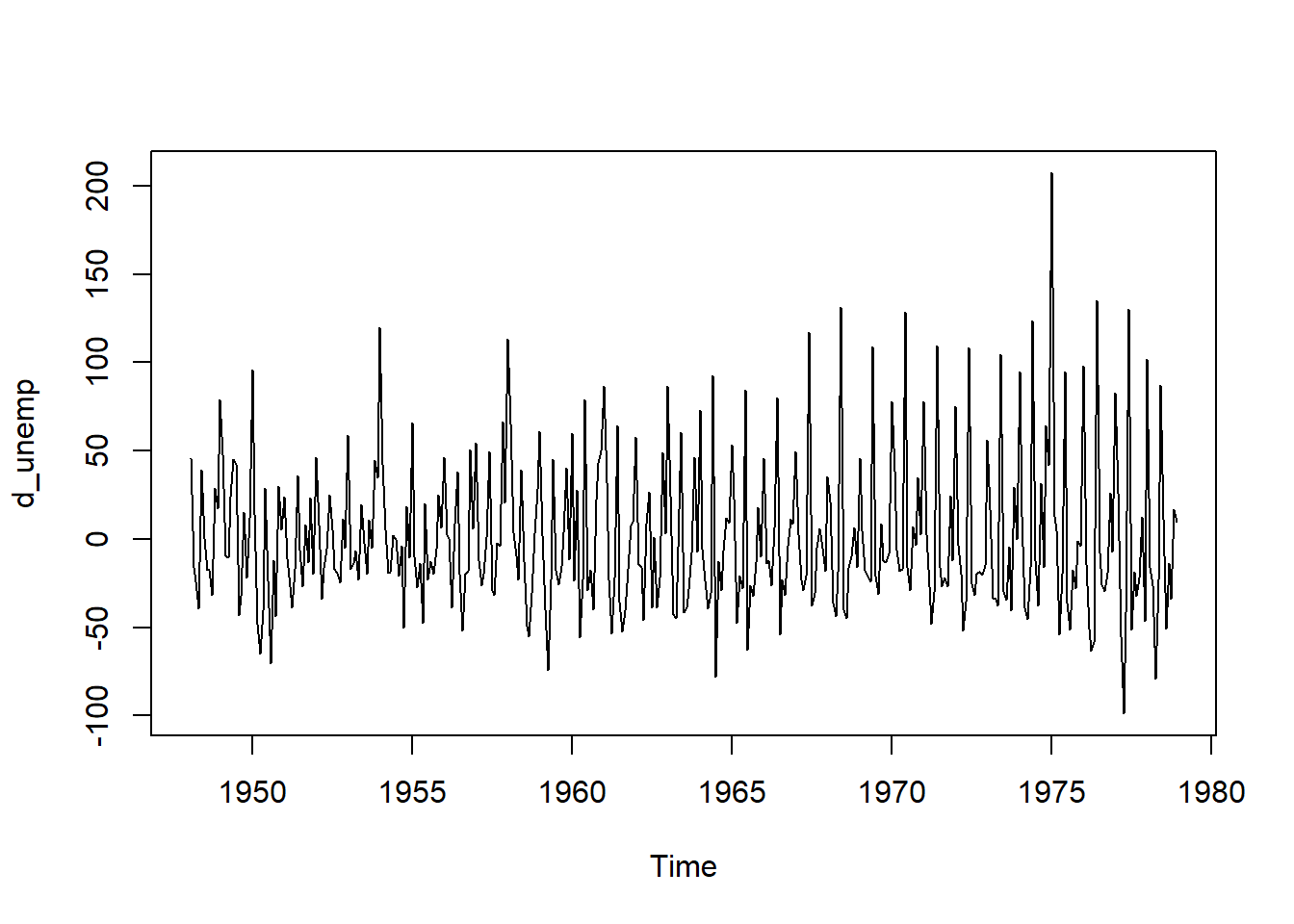

plot(unemp)

d_unemp <- diff(unemp)

plot(d_unemp)

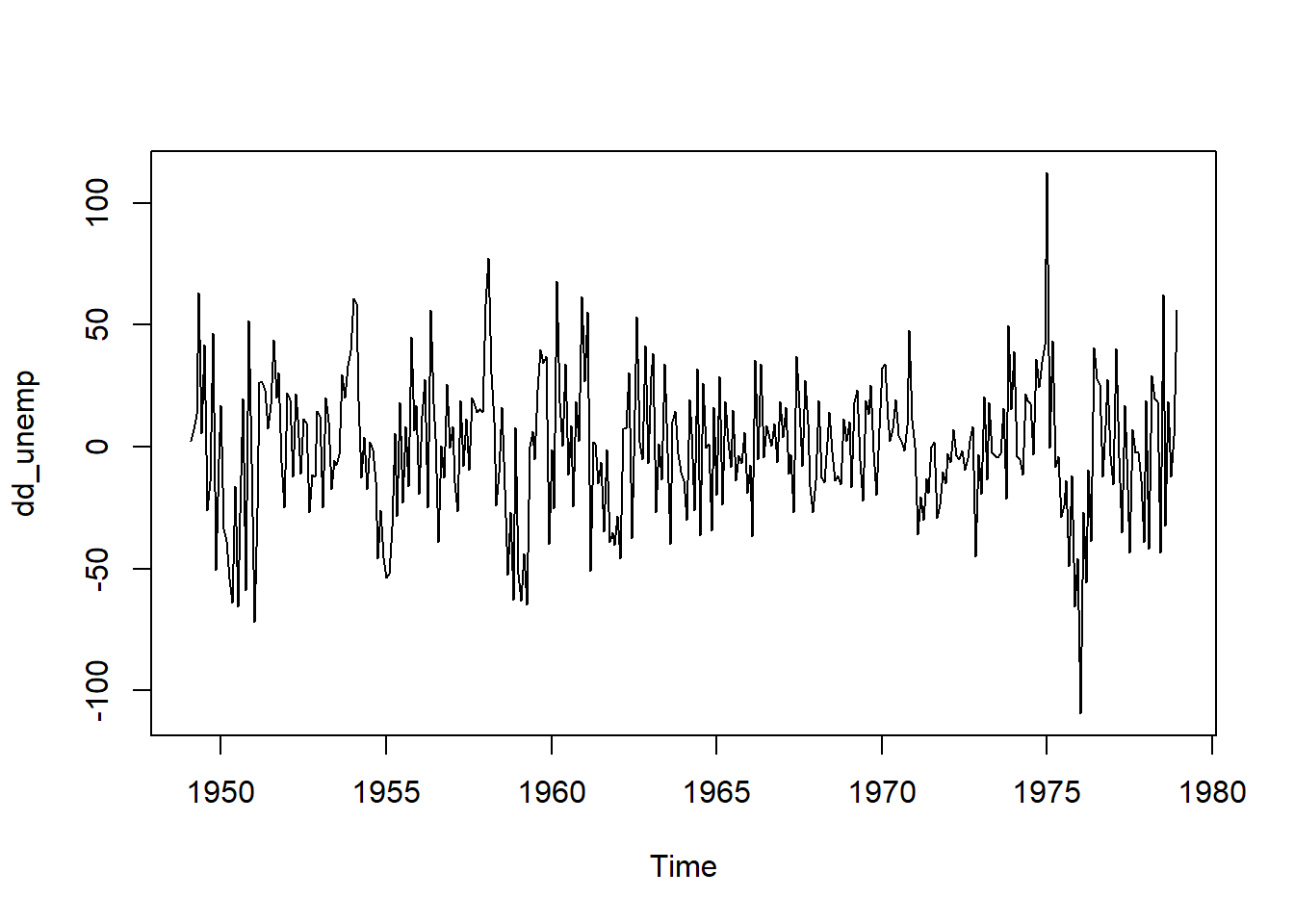

# Plot seasonal differenced diff_unemp

dd_unemp <- diff(d_unemp, lag = 12)

plot(dd_unemp)

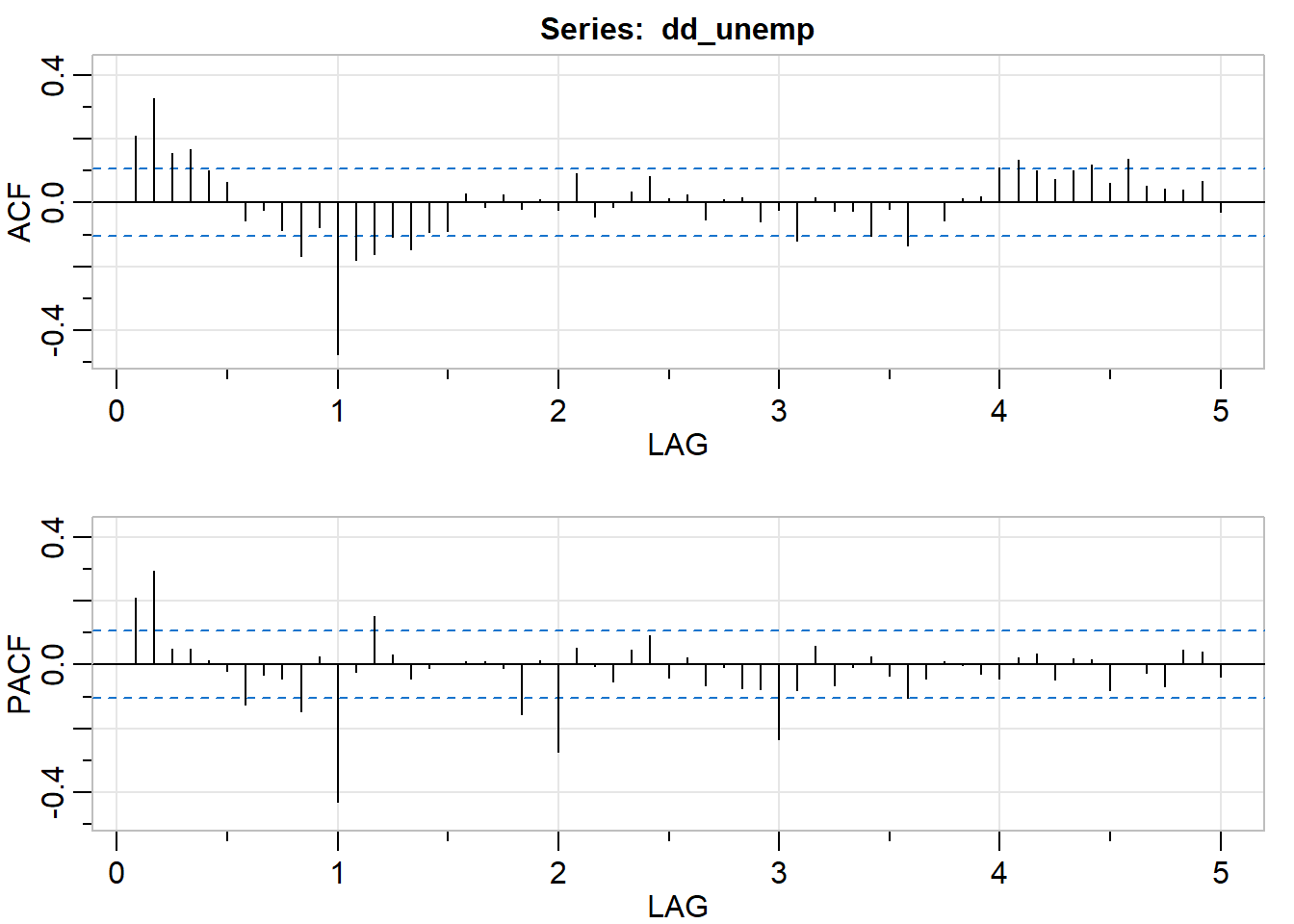

# Plot P/ACF pair of the fully differenced data to lag 60

dd_unemp <- diff(diff(unemp), lag = 12)

acf2(dd_unemp, max.lag = 60)

## [,1] [,2] [,3] [,4] [,5] [,6] [,7] [,8] [,9] [,10] [,11] [,12] [,13]

## ACF 0.21 0.33 0.15 0.17 0.10 0.06 -0.06 -0.02 -0.09 -0.17 -0.08 -0.48 -0.18

## PACF 0.21 0.29 0.05 0.05 0.01 -0.02 -0.12 -0.03 -0.05 -0.15 0.02 -0.43 -0.02

## [,14] [,15] [,16] [,17] [,18] [,19] [,20] [,21] [,22] [,23] [,24] [,25]

## ACF -0.16 -0.11 -0.15 -0.09 -0.09 0.03 -0.01 0.02 -0.02 0.01 -0.02 0.09

## PACF 0.15 0.03 -0.04 -0.01 0.00 0.01 0.01 -0.01 -0.16 0.01 -0.27 0.05

## [,26] [,27] [,28] [,29] [,30] [,31] [,32] [,33] [,34] [,35] [,36] [,37]

## ACF -0.05 -0.01 0.03 0.08 0.01 0.03 -0.05 0.01 0.02 -0.06 -0.02 -0.12

## PACF -0.01 -0.05 0.05 0.09 -0.04 0.02 -0.07 -0.01 -0.08 -0.08 -0.23 -0.08

## [,38] [,39] [,40] [,41] [,42] [,43] [,44] [,45] [,46] [,47] [,48] [,49]

## ACF 0.01 -0.03 -0.03 -0.10 -0.02 -0.13 0.00 -0.06 0.01 0.02 0.11 0.13

## PACF 0.06 -0.07 -0.01 0.03 -0.03 -0.11 -0.04 0.01 0.00 -0.03 -0.04 0.02

## [,50] [,51] [,52] [,53] [,54] [,55] [,56] [,57] [,58] [,59] [,60]

## ACF 0.10 0.07 0.10 0.12 0.06 0.14 0.05 0.04 0.04 0.07 -0.03

## PACF 0.03 -0.05 0.02 0.02 -0.08 0.00 -0.03 -0.07 0.05 0.04 -0.04# Fit an appropriate model

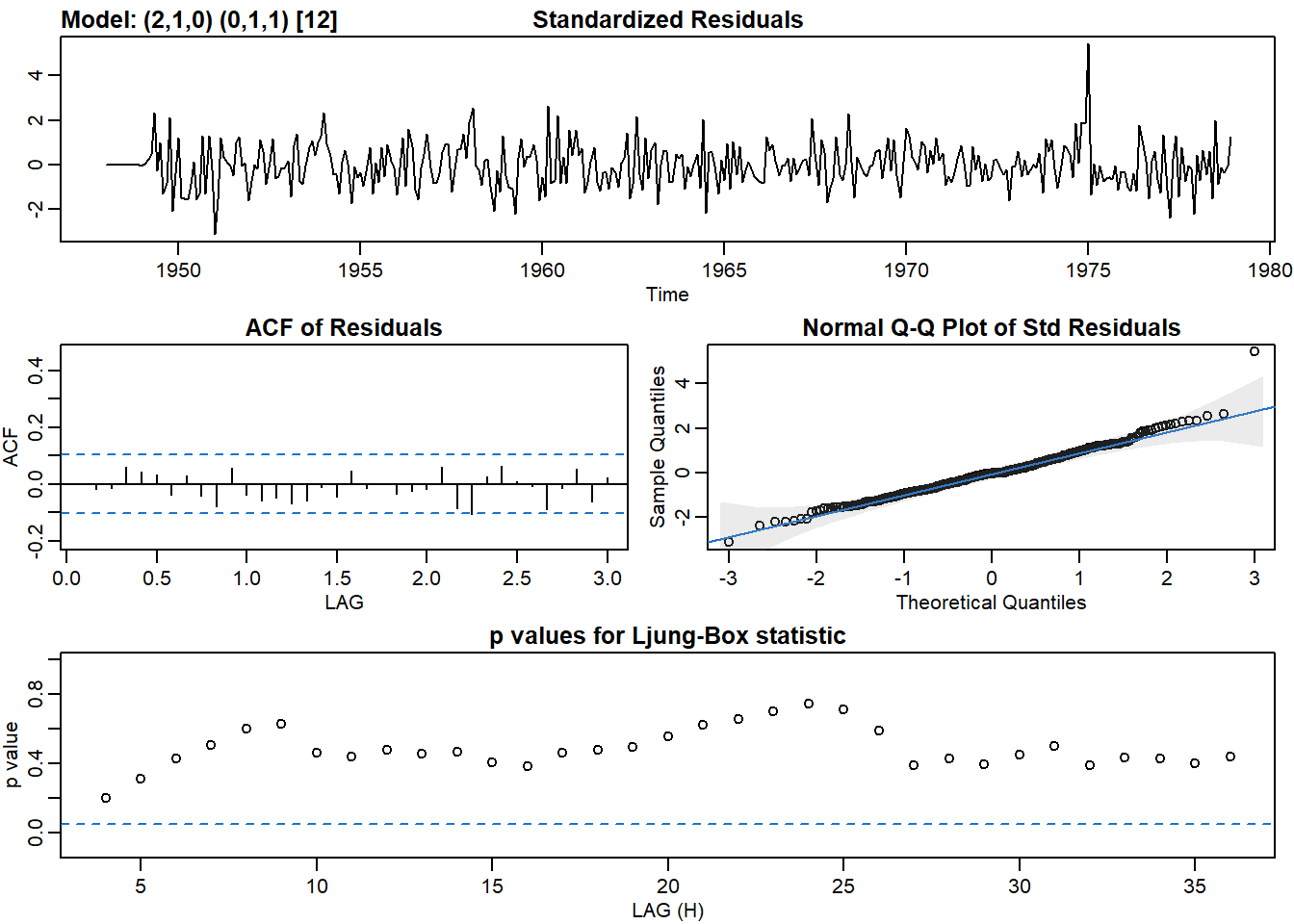

sarima(unemp, p = 2, d = 1, q = 0, P = 0, D = 1, Q = 1, S = 12)## initial value 3.340809

## iter 2 value 3.105512

## iter 3 value 3.086631

## iter 4 value 3.079778

## iter 5 value 3.069447

## iter 6 value 3.067659

## iter 7 value 3.067426

## iter 8 value 3.067418

## iter 8 value 3.067418

## final value 3.067418

## converged

## initial value 3.065481

## iter 2 value 3.065478

## iter 3 value 3.065477

## iter 3 value 3.065477

## iter 3 value 3.065477

## final value 3.065477

## converged

## $fit

##

## Call:

## stats::arima(x = xdata, order = c(p, d, q), seasonal = list(order = c(P, D,

## Q), period = S), include.mean = !no.constant, transform.pars = trans, fixed = fixed,

## optim.control = list(trace = trc, REPORT = 1, reltol = tol))

##

## Coefficients:

## ar1 ar2 sma1

## 0.1351 0.2464 -0.6953

## s.e. 0.0513 0.0515 0.0381

##

## sigma^2 estimated as 449.6: log likelihood = -1609.91, aic = 3227.81

##

## $degrees_of_freedom

## [1] 356

##

## $ttable

## Estimate SE t.value p.value

## ar1 0.1351 0.0513 2.6326 0.0088

## ar2 0.2464 0.0515 4.7795 0.0000

## sma1 -0.6953 0.0381 -18.2362 0.0000

##

## $AIC

## [1] 8.723811

##

## $AICc

## [1] 8.723988

##

## $BIC

## [1] 8.765793