12 Chapter 6 Lab

12.1 Forecasting with ARIMA

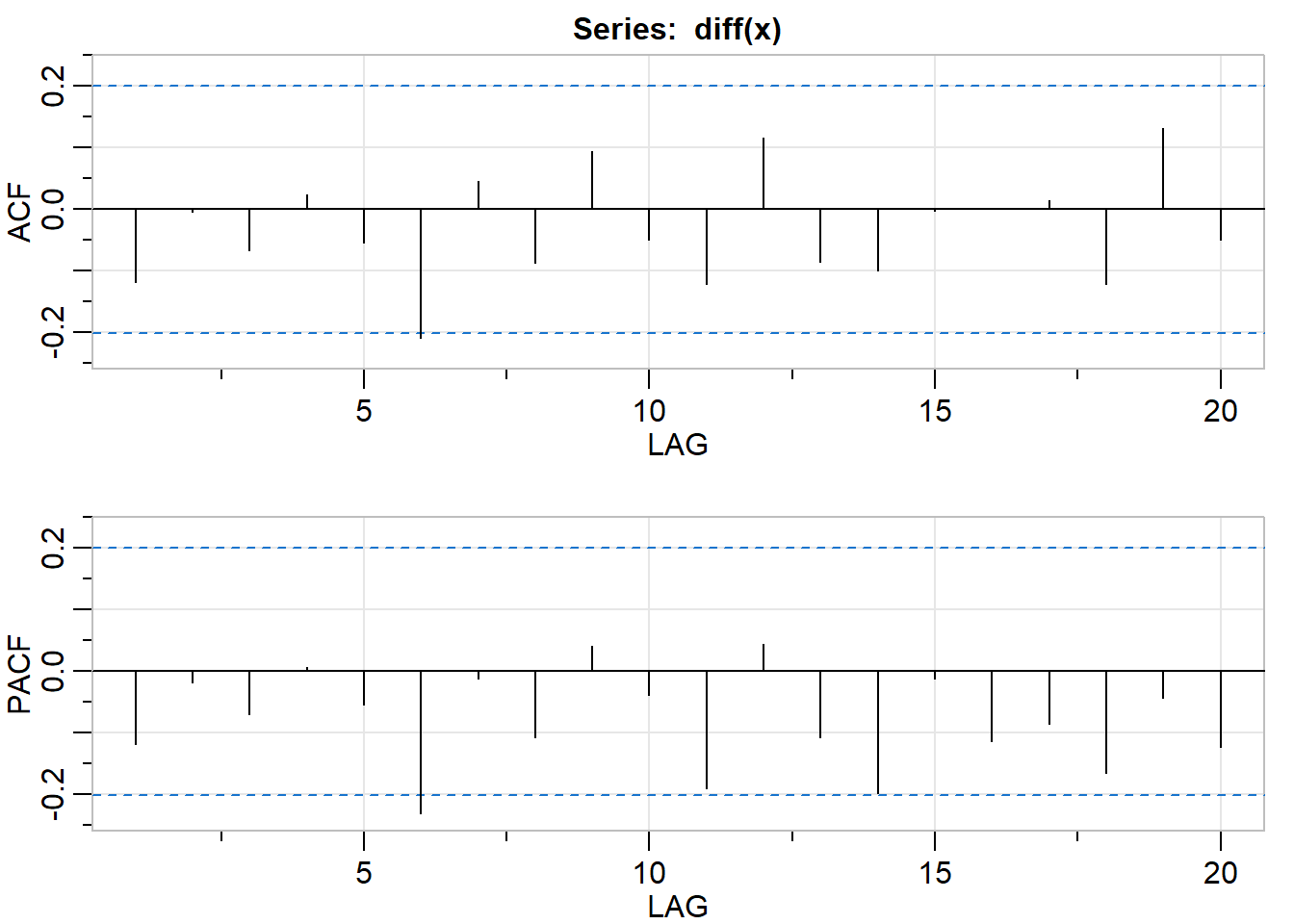

library(astsa)# Plot P/ACF pair of differenced data

acf2(diff(x))

## [,1] [,2] [,3] [,4] [,5] [,6] [,7] [,8] [,9] [,10] [,11] [,12]

## ACF -0.12 0.00 -0.07 0.02 -0.06 -0.21 0.05 -0.09 0.09 -0.05 -0.12 0.12

## PACF -0.12 -0.02 -0.07 0.01 -0.05 -0.23 -0.01 -0.11 0.04 -0.04 -0.19 0.04

## [,13] [,14] [,15] [,16] [,17] [,18] [,19] [,20]

## ACF -0.09 -0.1 0.00 0.00 0.01 -0.12 0.13 -0.05

## PACF -0.11 -0.2 -0.01 -0.11 -0.09 -0.17 -0.04 -0.12# Fit model - check t-table and diagnostics

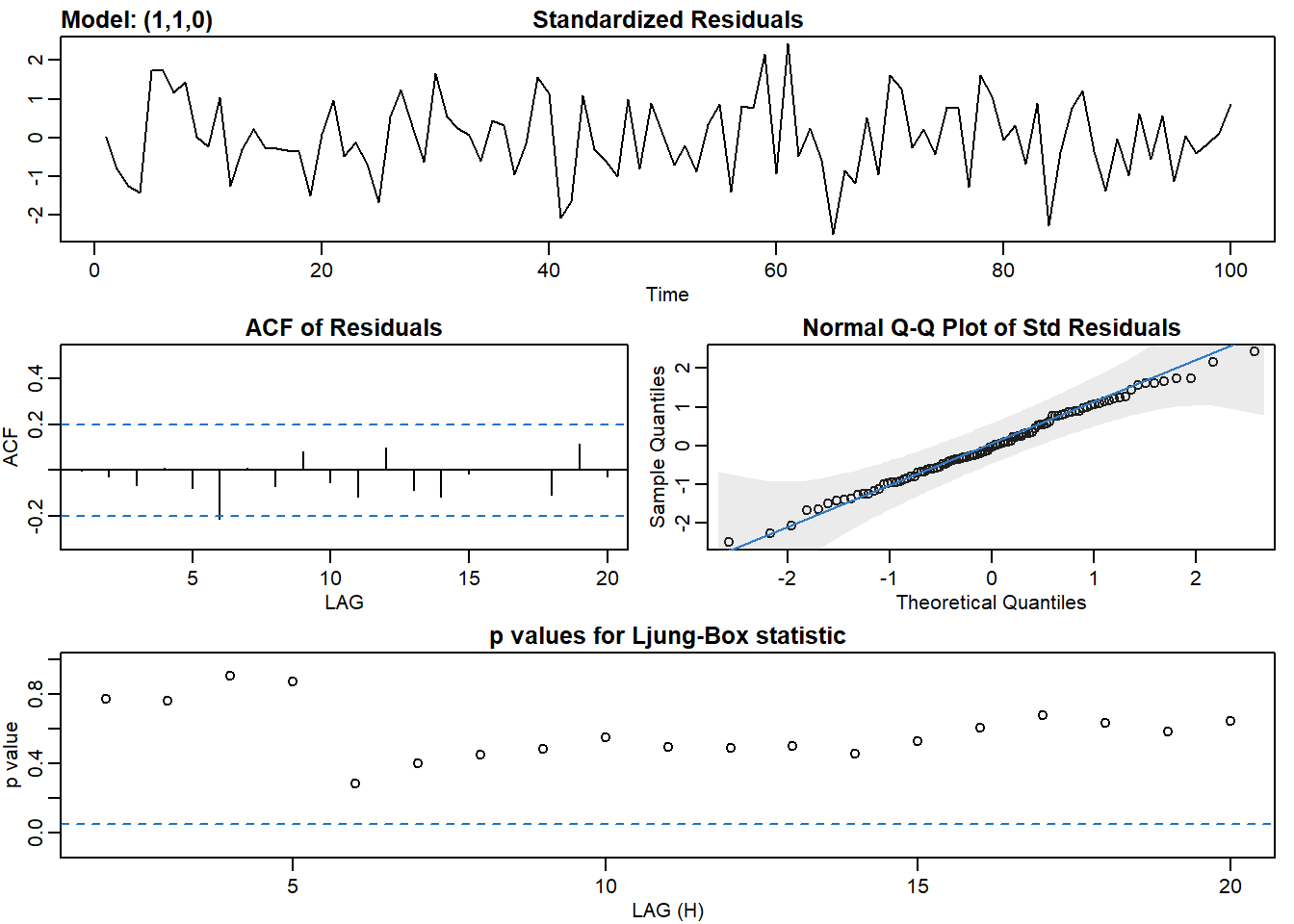

sarima(x, 1, 1, 0)## initial value 0.137947

## iter 2 value 0.130725

## iter 3 value 0.130723

## iter 4 value 0.130723

## iter 4 value 0.130723

## iter 4 value 0.130723

## final value 0.130723

## converged

## initial value 0.128980

## iter 2 value 0.128956

## iter 3 value 0.128954

## iter 3 value 0.128954

## iter 3 value 0.128954

## final value 0.128954

## converged

## $fit

##

## Call:

## stats::arima(x = xdata, order = c(p, d, q), seasonal = list(order = c(P, D,

## Q), period = S), xreg = constant, transform.pars = trans, fixed = fixed,

## optim.control = list(trace = trc, REPORT = 1, reltol = tol))

##

## Coefficients:

## ar1 constant

## -0.1192 0.0788

## s.e. 0.1000 0.1023

##

## sigma^2 estimated as 1.294: log likelihood = -153.24, aic = 312.48

##

## $degrees_of_freedom

## [1] 97

##

## $ttable

## Estimate SE t.value p.value

## ar1 -0.1192 0.1000 -1.1921 0.2361

## constant 0.0788 0.1023 0.7707 0.4428

##

## $AIC

## [1] 3.156391

##

## $AICc

## [1] 3.157653

##

## $BIC

## [1] 3.235031# Forecast the data 20 time periods ahead

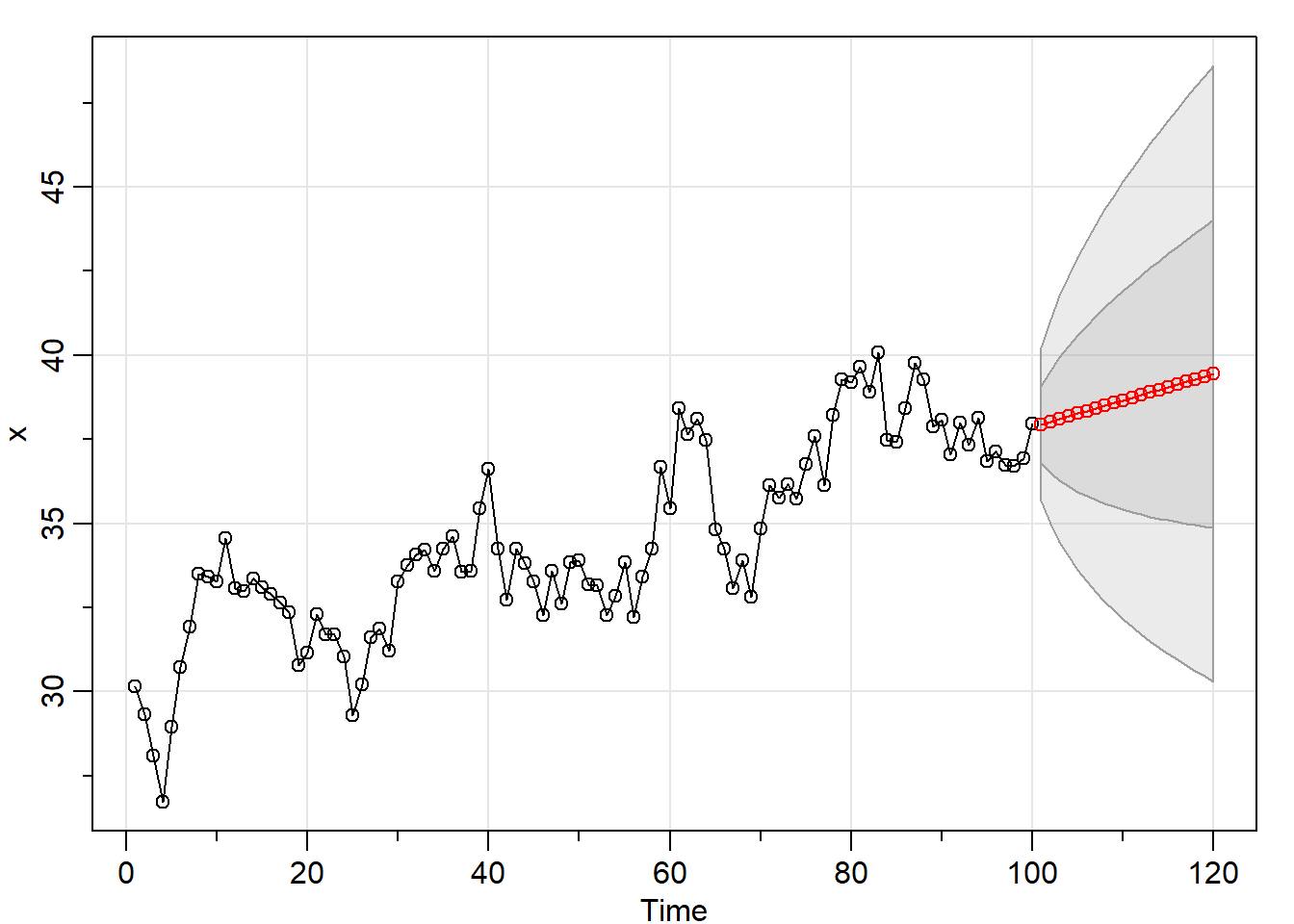

sarima.for(x, n.ahead = 20, p = 1, d = 1, q = 0)

## $pred

## Time Series:

## Start = 101

## End = 120

## Frequency = 1

## [1] 37.93860 38.03106 38.10825 38.18726 38.26606 38.34488 38.42369 38.50251

## [9] 38.58133 38.66015 38.73897 38.81778 38.89660 38.97542 39.05424 39.13306

## [17] 39.21187 39.29069 39.36951 39.44833

##

## $se

## Time Series:

## Start = 101

## End = 120

## Frequency = 1

## [1] 1.137555 1.515934 1.826118 2.089843 2.323929 2.536493 2.732572 2.915493

## [9] 3.087597 3.250601 3.405813 3.554253 3.696737 3.833930 3.966381 4.094549

## [17] 4.218825 4.339543 4.456993 4.57142712.2 Global Temp data

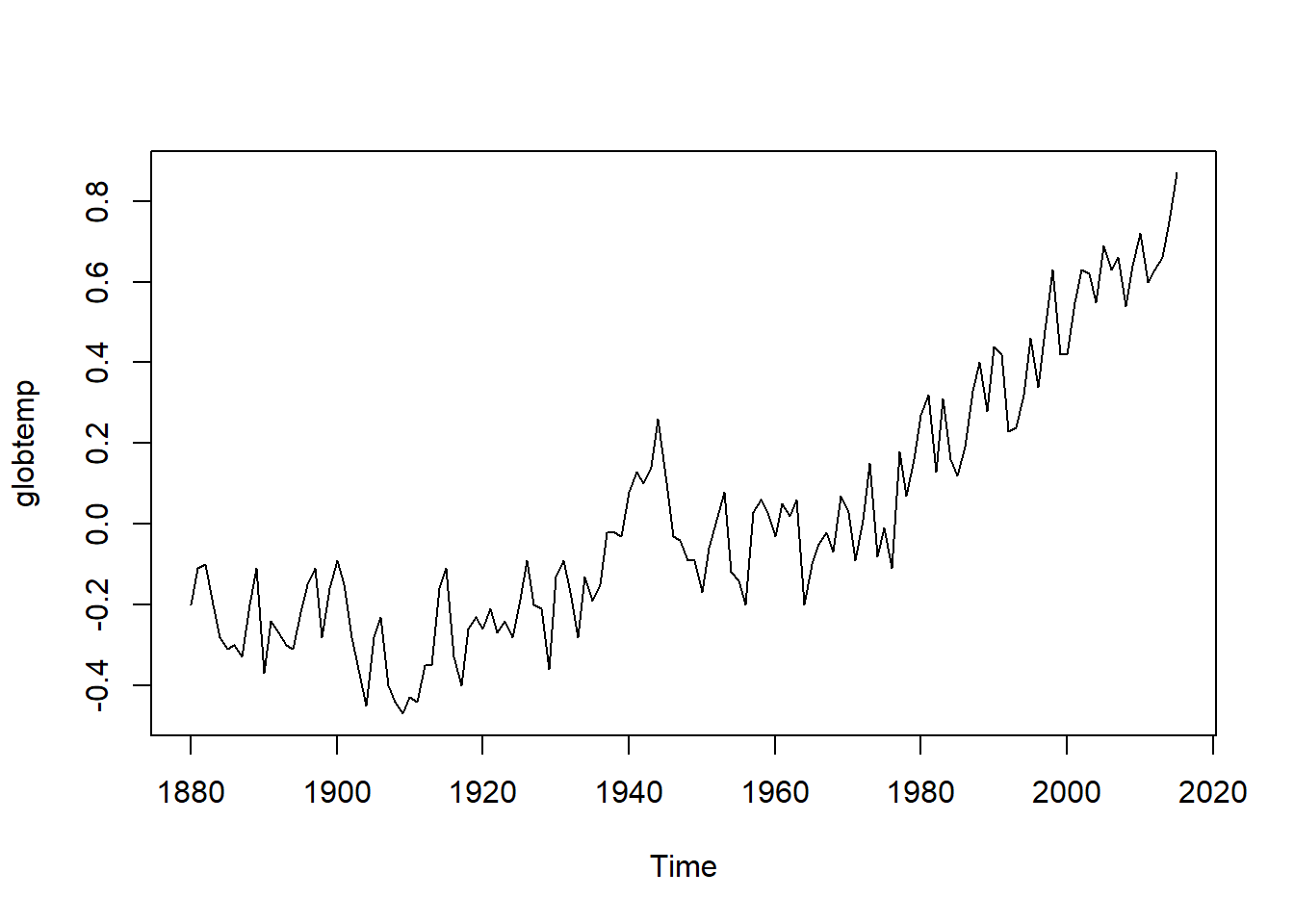

head(globtemp)## [1] -0.20 -0.11 -0.10 -0.20 -0.28 -0.31plot(globtemp)

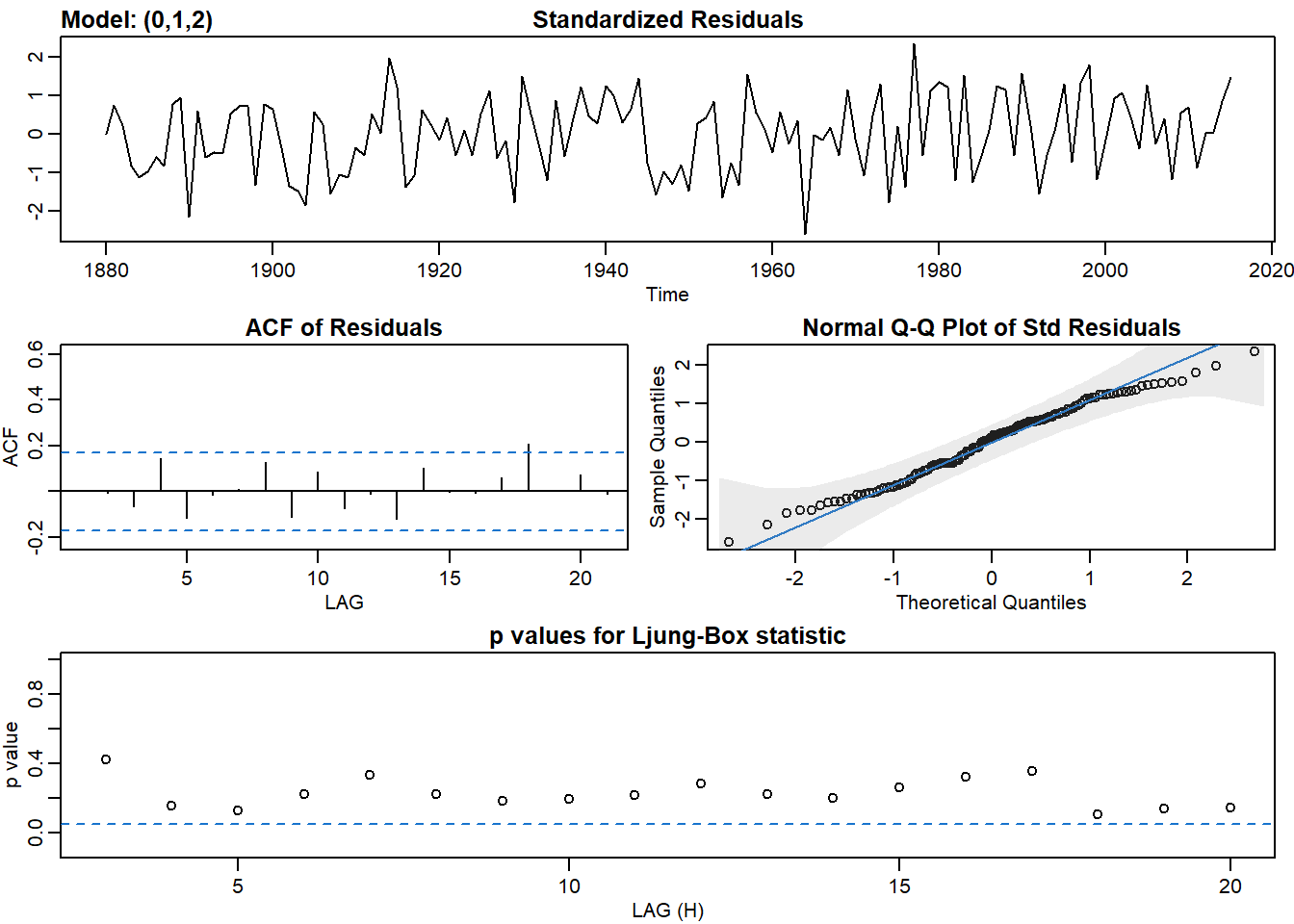

# Fit an ARIMA(0,1,2) to globtemp and check the fit

sarima(globtemp, 0,1,2)## initial value -2.220513

## iter 2 value -2.294887

## iter 3 value -2.307682

## iter 4 value -2.309170

## iter 5 value -2.310360

## iter 6 value -2.311251

## iter 7 value -2.311636

## iter 8 value -2.311648

## iter 9 value -2.311649

## iter 9 value -2.311649

## iter 9 value -2.311649

## final value -2.311649

## converged

## initial value -2.310187

## iter 2 value -2.310197

## iter 3 value -2.310199

## iter 4 value -2.310201

## iter 5 value -2.310202

## iter 5 value -2.310202

## iter 5 value -2.310202

## final value -2.310202

## converged

## $fit

##

## Call:

## stats::arima(x = xdata, order = c(p, d, q), seasonal = list(order = c(P, D,

## Q), period = S), xreg = constant, transform.pars = trans, fixed = fixed,

## optim.control = list(trace = trc, REPORT = 1, reltol = tol))

##

## Coefficients:

## ma1 ma2 constant

## -0.3984 -0.2173 0.0072

## s.e. 0.0808 0.0768 0.0033

##

## sigma^2 estimated as 0.00982: log likelihood = 120.32, aic = -232.64

##

## $degrees_of_freedom

## [1] 132

##

## $ttable

## Estimate SE t.value p.value

## ma1 -0.3984 0.0808 -4.9313 0.0000

## ma2 -0.2173 0.0768 -2.8303 0.0054

## constant 0.0072 0.0033 2.1463 0.0337

##

## $AIC

## [1] -1.723268

##

## $AICc

## [1] -1.721911

##

## $BIC

## [1] -1.637185# Forecast data 35 years into the future

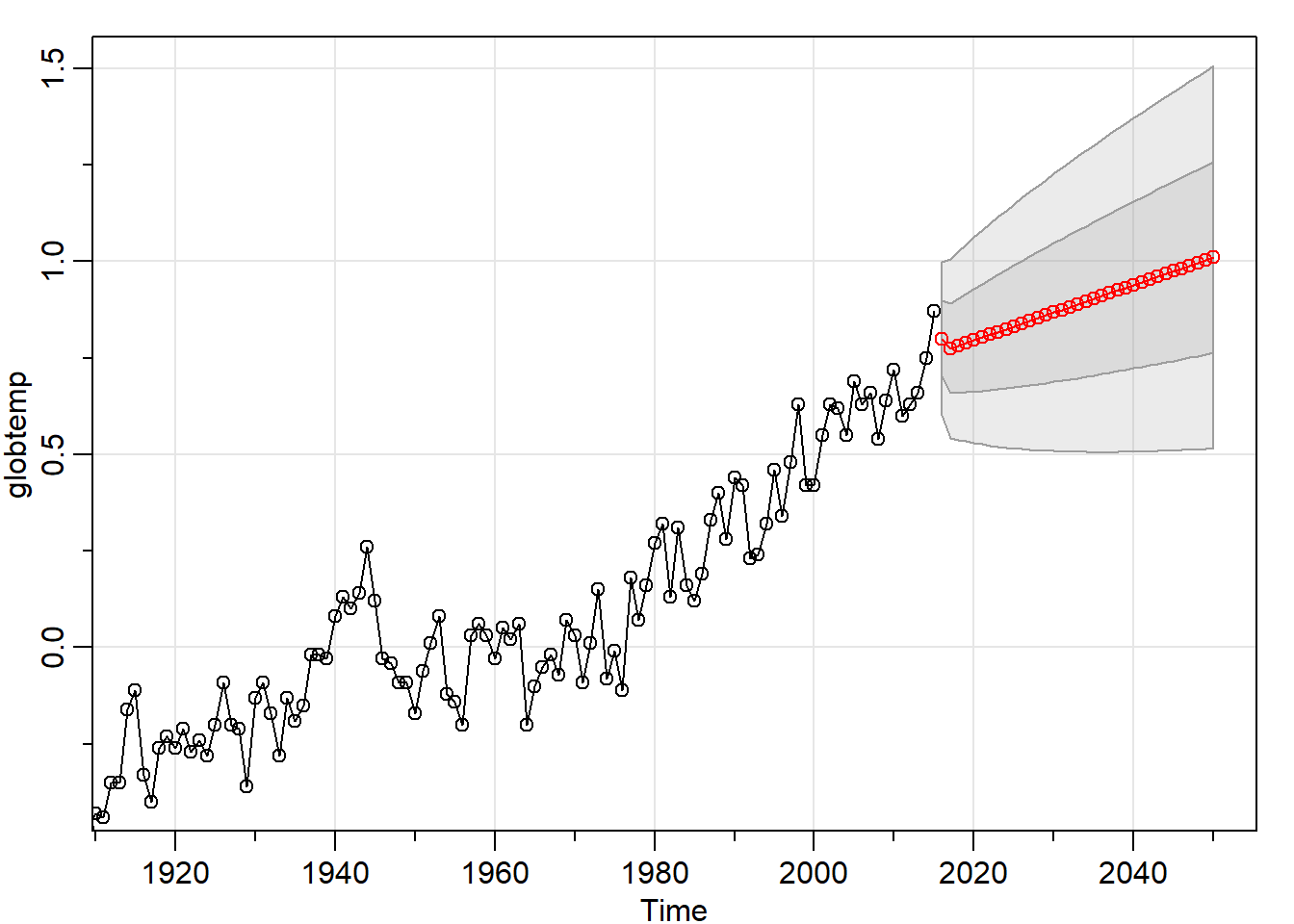

sarima.for(globtemp, 35, 0,1,2)

## $pred

## Time Series:

## Start = 2016

## End = 2050

## Frequency = 1

## [1] 0.7995567 0.7745381 0.7816919 0.7888457 0.7959996 0.8031534 0.8103072

## [8] 0.8174611 0.8246149 0.8317688 0.8389226 0.8460764 0.8532303 0.8603841

## [15] 0.8675379 0.8746918 0.8818456 0.8889995 0.8961533 0.9033071 0.9104610

## [22] 0.9176148 0.9247687 0.9319225 0.9390763 0.9462302 0.9533840 0.9605378

## [29] 0.9676917 0.9748455 0.9819994 0.9891532 0.9963070 1.0034609 1.0106147

##

## $se

## Time Series:

## Start = 2016

## End = 2050

## Frequency = 1

## [1] 0.09909556 0.11564576 0.12175580 0.12757353 0.13313729 0.13847769

## [7] 0.14361964 0.14858376 0.15338730 0.15804492 0.16256915 0.16697084

## [13] 0.17125943 0.17544322 0.17952954 0.18352490 0.18743511 0.19126540

## [19] 0.19502047 0.19870459 0.20232164 0.20587515 0.20936836 0.21280424

## [25] 0.21618551 0.21951471 0.22279416 0.22602604 0.22921235 0.23235497

## [31] 0.23545565 0.23851603 0.24153763 0.24452190 0.24747019Pure seasonal model takes 4 more parameters P, S, D, Q

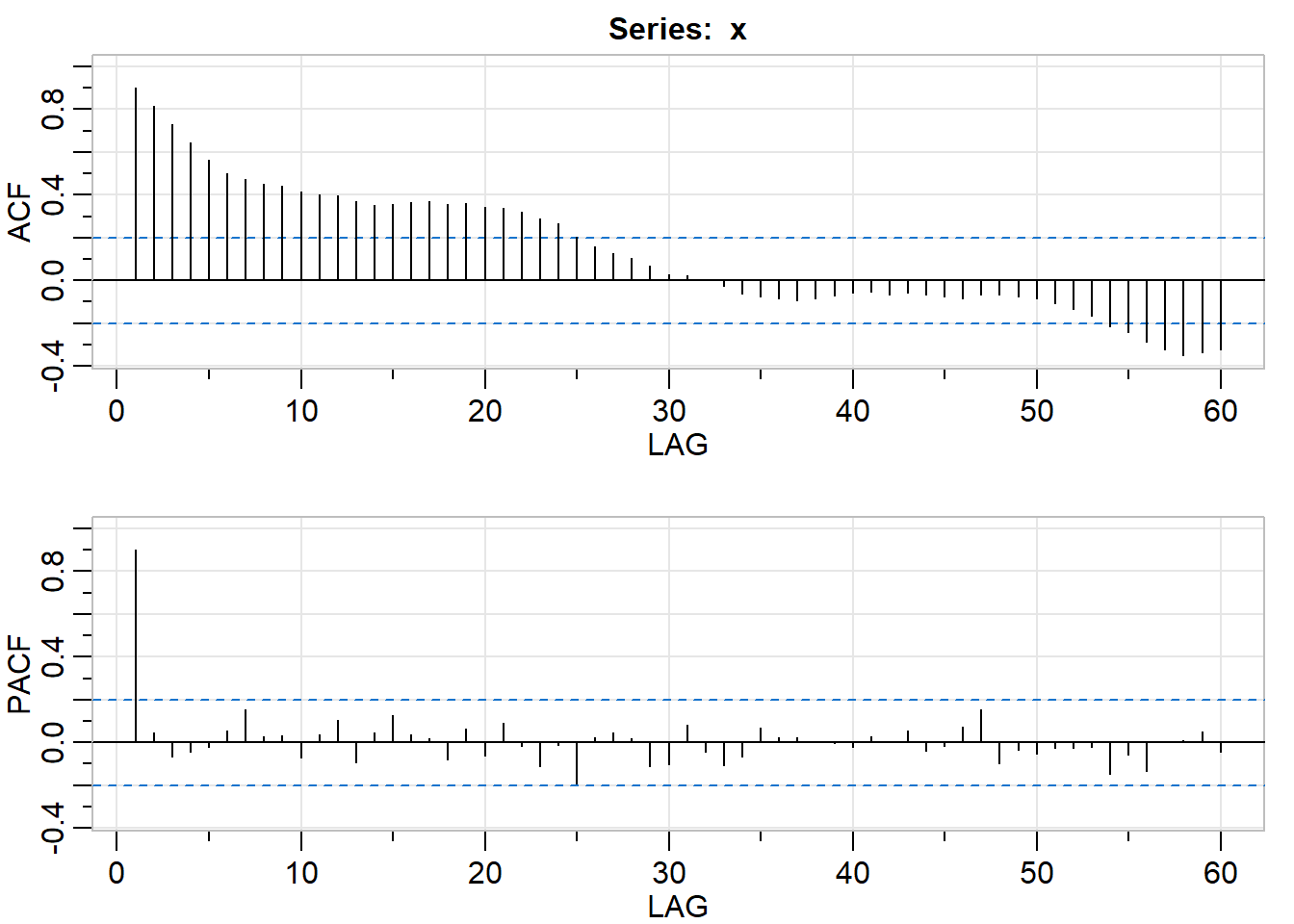

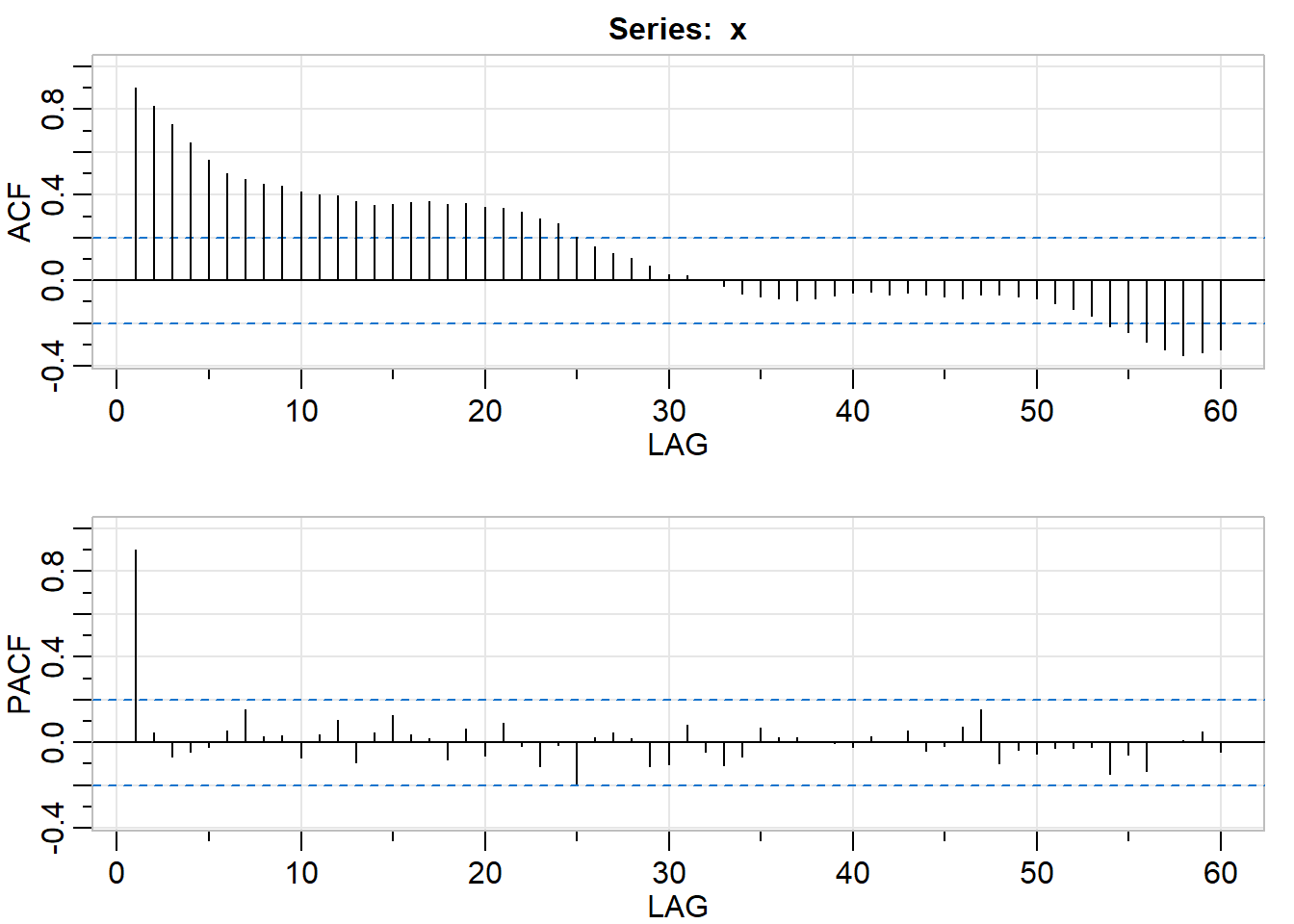

# Plot sample P/ACF to lag 60 and compare to the true values

acf2(x, max.lag = 60)

## [,1] [,2] [,3] [,4] [,5] [,6] [,7] [,8] [,9] [,10] [,11] [,12] [,13]

## ACF 0.9 0.82 0.73 0.64 0.56 0.50 0.48 0.45 0.44 0.42 0.40 0.4 0.37

## PACF 0.9 0.04 -0.07 -0.04 -0.02 0.05 0.15 0.03 0.03 -0.07 0.04 0.1 -0.09

## [,14] [,15] [,16] [,17] [,18] [,19] [,20] [,21] [,22] [,23] [,24] [,25]

## ACF 0.35 0.36 0.36 0.37 0.36 0.36 0.34 0.34 0.32 0.29 0.27 0.20

## PACF 0.05 0.13 0.04 0.02 -0.08 0.06 -0.06 0.09 -0.02 -0.11 -0.01 -0.19

## [,26] [,27] [,28] [,29] [,30] [,31] [,32] [,33] [,34] [,35] [,36] [,37]

## ACF 0.16 0.12 0.10 0.07 0.03 0.02 0.00 -0.03 -0.06 -0.08 -0.08 -0.09

## PACF 0.02 0.04 0.02 -0.11 -0.10 0.08 -0.04 -0.11 -0.07 0.07 0.02 0.02

## [,38] [,39] [,40] [,41] [,42] [,43] [,44] [,45] [,46] [,47] [,48] [,49]

## ACF -0.09 -0.07 -0.06 -0.05 -0.07 -0.06 -0.07 -0.08 -0.08 -0.07 -0.07 -0.07

## PACF 0.01 0.00 -0.02 0.03 0.00 0.06 -0.04 -0.02 0.07 0.15 -0.10 -0.04

## [,50] [,51] [,52] [,53] [,54] [,55] [,56] [,57] [,58] [,59] [,60]

## ACF -0.08 -0.11 -0.13 -0.17 -0.21 -0.24 -0.29 -0.32 -0.35 -0.34 -0.32

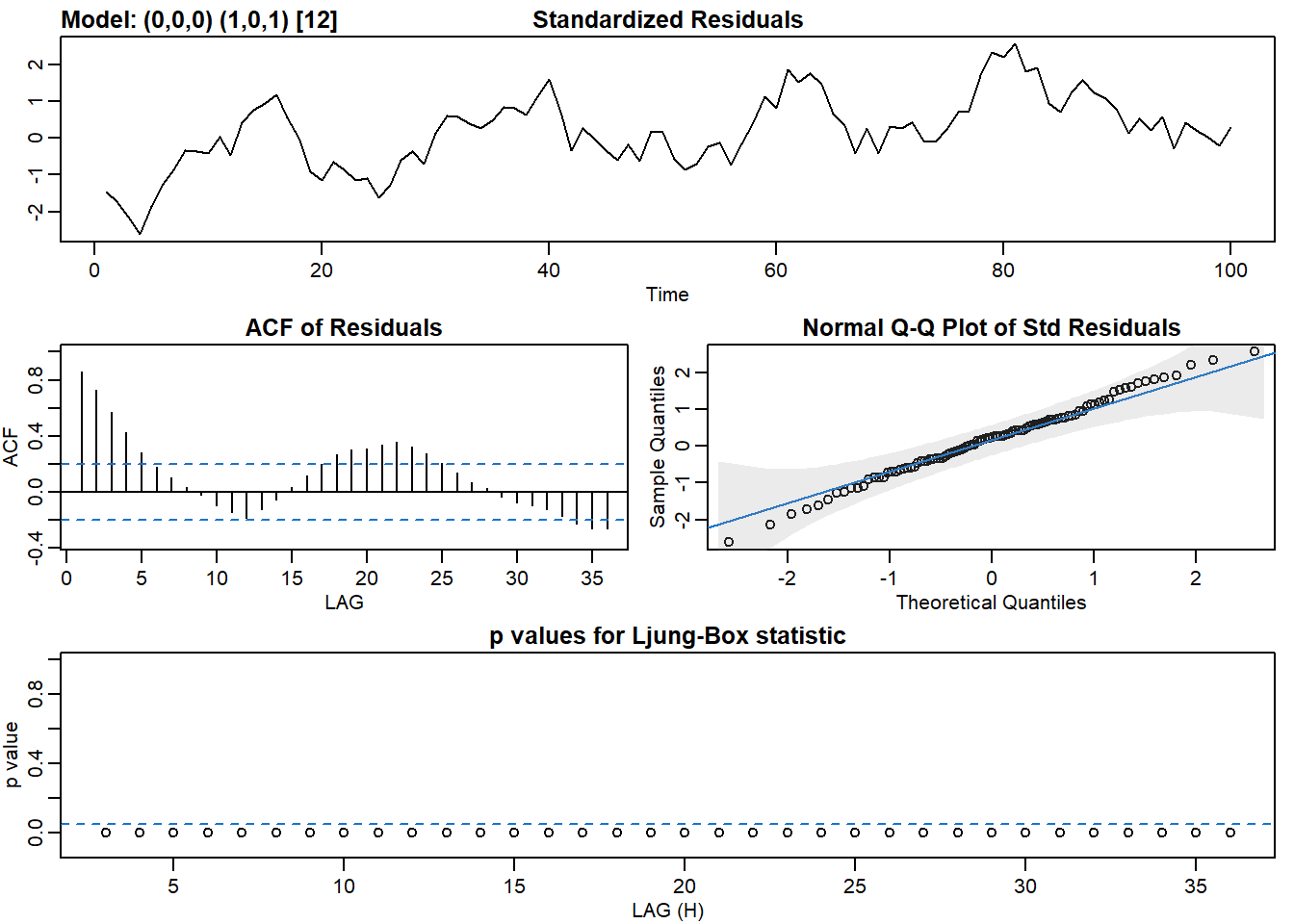

## PACF -0.05 -0.03 -0.02 -0.02 -0.15 -0.06 -0.13 0.00 0.01 0.05 -0.05# Fit the seasonal model to x

sarima(x, p = 0, d = 0, q = 0, P = 1, D = 0, Q = 1, S = 12)## initial value 0.958236

## iter 2 value 0.876547

## iter 3 value 0.812976

## iter 4 value 0.777142

## iter 5 value 0.747937

## iter 6 value 0.725263

## iter 7 value 0.719720

## iter 8 value 0.693755

## iter 9 value 0.690447

## iter 10 value 0.681477

## iter 11 value 0.680611

## iter 12 value 0.680126

## iter 13 value 0.679664

## iter 14 value 0.678787

## iter 15 value 0.678244

## iter 16 value 0.678215

## iter 17 value 0.678182

## iter 18 value 0.678167

## iter 19 value 0.678158

## iter 20 value 0.678128

## iter 21 value 0.678102

## iter 22 value 0.678085

## iter 23 value 0.678084

## iter 24 value 0.678084

## iter 25 value 0.678083

## iter 26 value 0.678083

## iter 27 value 0.678083

## iter 28 value 0.678083

## iter 29 value 0.678083

## iter 29 value 0.678083

## final value 0.678083

## converged

## initial value 1.316632

## iter 2 value 1.078864

## iter 3 value 1.008425

## iter 4 value 0.990485

## iter 5 value 0.972791

## iter 6 value 0.957820

## iter 7 value 0.946498

## iter 8 value 0.936672

## iter 9 value 0.929951

## iter 10 value 0.915219

## iter 11 value 0.913770

## iter 12 value 0.904973

## iter 13 value 0.903657

## iter 14 value 0.903549

## iter 15 value 0.903545

## iter 16 value 0.903544

## iter 17 value 0.903543

## iter 18 value 0.903542

## iter 19 value 0.903542

## iter 19 value 0.903542

## iter 19 value 0.903542

## final value 0.903542

## converged

## $fit

##

## Call:

## stats::arima(x = xdata, order = c(p, d, q), seasonal = list(order = c(P, D,

## Q), period = S), xreg = xmean, include.mean = FALSE, transform.pars = trans,

## fixed = fixed, optim.control = list(trace = trc, REPORT = 1, reltol = tol))

##

## Coefficients:

## sar1 sma1 xmean

## 0.7141 -0.2117 34.4740

## s.e. 0.1099 0.1181 0.5357

##

## sigma^2 estimated as 5.785: log likelihood = -232.25, aic = 472.5

##

## $degrees_of_freedom

## [1] 97

##

## $ttable

## Estimate SE t.value p.value

## sar1 0.7141 0.1099 6.4973 0.0000

## sma1 -0.2117 0.1181 -1.7927 0.0761

## xmean 34.4740 0.5357 64.3483 0.0000

##

## $AIC

## [1] 4.724962

##

## $AICc

## [1] 4.727462

##

## $BIC

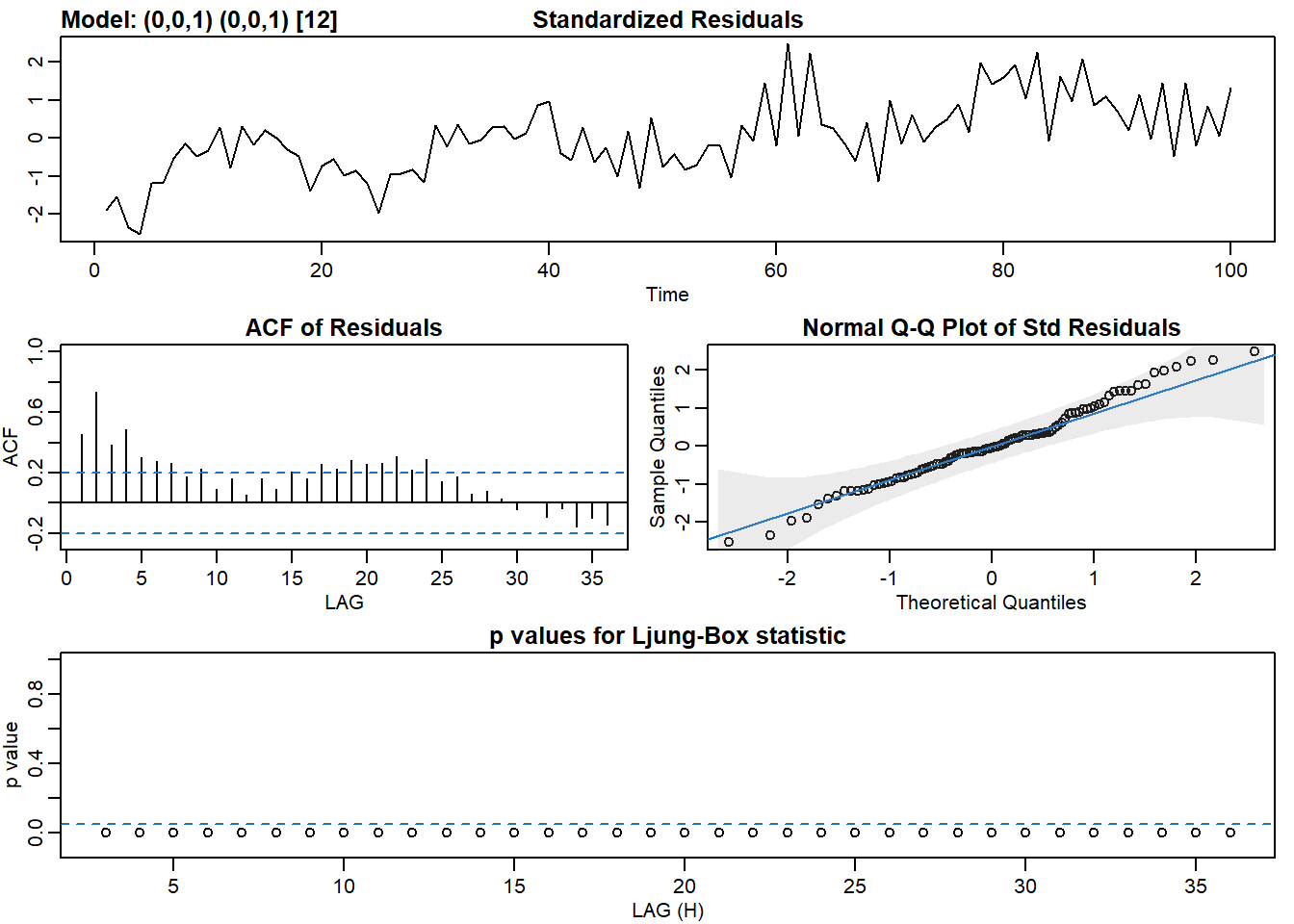

## [1] 4.829169However, pure seasonal won’t be likely. Data in real life will tend to be mixed seasonal model (specified p, d, q in addition to P, D, Q, S)

# Plot sample P/ACF pair to lag 60 and compare to actual

acf2(x, max.lag = 60)

## [,1] [,2] [,3] [,4] [,5] [,6] [,7] [,8] [,9] [,10] [,11] [,12] [,13]

## ACF 0.9 0.82 0.73 0.64 0.56 0.50 0.48 0.45 0.44 0.42 0.40 0.4 0.37

## PACF 0.9 0.04 -0.07 -0.04 -0.02 0.05 0.15 0.03 0.03 -0.07 0.04 0.1 -0.09

## [,14] [,15] [,16] [,17] [,18] [,19] [,20] [,21] [,22] [,23] [,24] [,25]

## ACF 0.35 0.36 0.36 0.37 0.36 0.36 0.34 0.34 0.32 0.29 0.27 0.20

## PACF 0.05 0.13 0.04 0.02 -0.08 0.06 -0.06 0.09 -0.02 -0.11 -0.01 -0.19

## [,26] [,27] [,28] [,29] [,30] [,31] [,32] [,33] [,34] [,35] [,36] [,37]

## ACF 0.16 0.12 0.10 0.07 0.03 0.02 0.00 -0.03 -0.06 -0.08 -0.08 -0.09

## PACF 0.02 0.04 0.02 -0.11 -0.10 0.08 -0.04 -0.11 -0.07 0.07 0.02 0.02

## [,38] [,39] [,40] [,41] [,42] [,43] [,44] [,45] [,46] [,47] [,48] [,49]

## ACF -0.09 -0.07 -0.06 -0.05 -0.07 -0.06 -0.07 -0.08 -0.08 -0.07 -0.07 -0.07

## PACF 0.01 0.00 -0.02 0.03 0.00 0.06 -0.04 -0.02 0.07 0.15 -0.10 -0.04

## [,50] [,51] [,52] [,53] [,54] [,55] [,56] [,57] [,58] [,59] [,60]

## ACF -0.08 -0.11 -0.13 -0.17 -0.21 -0.24 -0.29 -0.32 -0.35 -0.34 -0.32

## PACF -0.05 -0.03 -0.02 -0.02 -0.15 -0.06 -0.13 0.00 0.01 0.05 -0.05# Fit the seasonal model to x

sarima(x, p = 0, d = 0, q = 1, P = 0, D = 0, Q = 1, S = 12)## initial value 1.040726

## iter 2 value 0.685896

## iter 3 value 0.666207

## iter 4 value 0.607557

## iter 5 value 0.602804

## iter 6 value 0.596031

## iter 7 value 0.595761

## iter 8 value 0.595755

## iter 9 value 0.595754

## iter 10 value 0.595754

## iter 11 value 0.595754

## iter 12 value 0.595754

## iter 12 value 0.595754

## iter 12 value 0.595754

## final value 0.595754

## converged

## initial value 0.588139

## iter 2 value 0.587695

## iter 3 value 0.587540

## iter 4 value 0.587468

## iter 5 value 0.587440

## iter 6 value 0.587440

## iter 7 value 0.587440

## iter 7 value 0.587440

## iter 7 value 0.587440

## final value 0.587440

## converged

## $fit

##

## Call:

## stats::arima(x = xdata, order = c(p, d, q), seasonal = list(order = c(P, D,

## Q), period = S), xreg = xmean, include.mean = FALSE, transform.pars = trans,

## fixed = fixed, optim.control = list(trace = trc, REPORT = 1, reltol = tol))

##

## Coefficients:

## ma1 sma1 xmean

## 0.7270 0.2512 34.4628

## s.e. 0.0588 0.0803 0.3758

##

## sigma^2 estimated as 3.189: log likelihood = -200.64, aic = 409.28

##

## $degrees_of_freedom

## [1] 97

##

## $ttable

## Estimate SE t.value p.value

## ma1 0.7270 0.0588 12.3579 0.0000

## sma1 0.2512 0.0803 3.1284 0.0023

## xmean 34.4628 0.3758 91.7171 0.0000

##

## $AIC

## [1] 4.092756

##

## $AICc

## [1] 4.095256

##

## $BIC

## [1] 4.19696312.3 Exponential smoothing

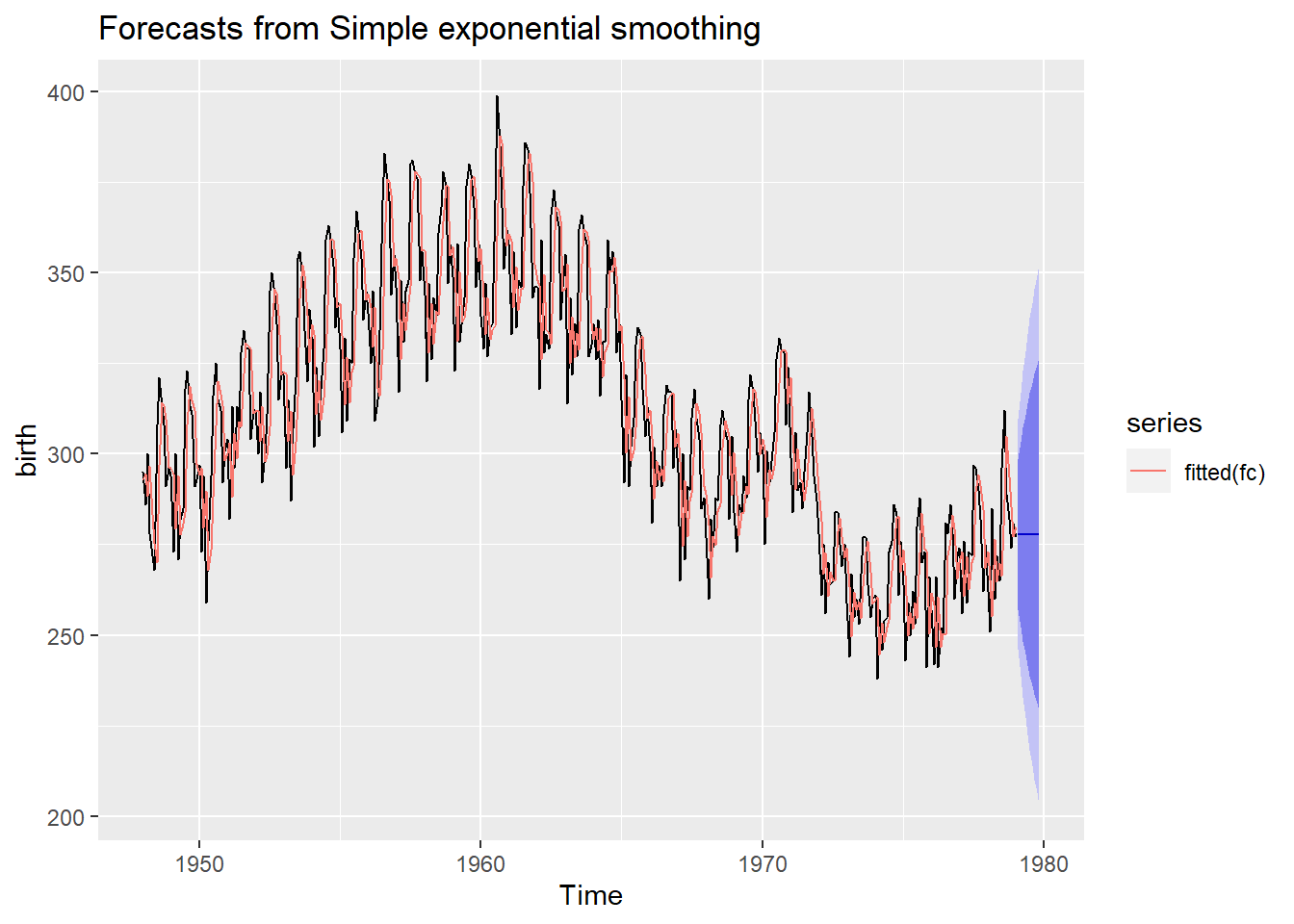

library(forecast)

fc <- ses(birth, h = 10)

summary(fc)##

## Forecast method: Simple exponential smoothing

##

## Model Information:

## Simple exponential smoothing

##

## Call:

## ses(y = birth, h = 10)

##

## Smoothing parameters:

## alpha = 0.7106

##

## Initial states:

## l = 292.9802

##

## sigma: 16.2158

##

## AIC AICc BIC

## 4291.087 4291.152 4302.851

##

## Error measures:

## ME RMSE MAE MPE MAPE MASE ACF1

## Training set -0.0570963 16.17222 13.034 -0.195208 4.228966 1.328423 -0.02023071

##

## Forecasts:

## Point Forecast Lo 80 Hi 80 Lo 95 Hi 95

## Feb 1979 277.8466 257.0653 298.6279 246.0643 309.6289

## Mar 1979 277.8466 252.3528 303.3404 238.8572 316.8360

## Apr 1979 277.8466 248.3847 307.3085 232.7885 322.9047

## May 1979 277.8466 244.8910 310.8022 227.4453 328.2479

## Jun 1979 277.8466 241.7337 313.9595 222.6167 333.0765

## Jul 1979 277.8466 238.8311 316.8621 218.1775 337.5157

## Aug 1979 277.8466 236.1299 319.5633 214.0464 341.6468

## Sep 1979 277.8466 233.5933 322.0999 210.1671 345.5261

## Oct 1979 277.8466 231.1945 324.4987 206.4983 349.1949

## Nov 1979 277.8466 228.9131 326.7801 203.0092 352.6840autoplot(fc)

# Add the one-step forecasts for the training data to the plot

autoplot(fc) + autolayer(fitted(fc))

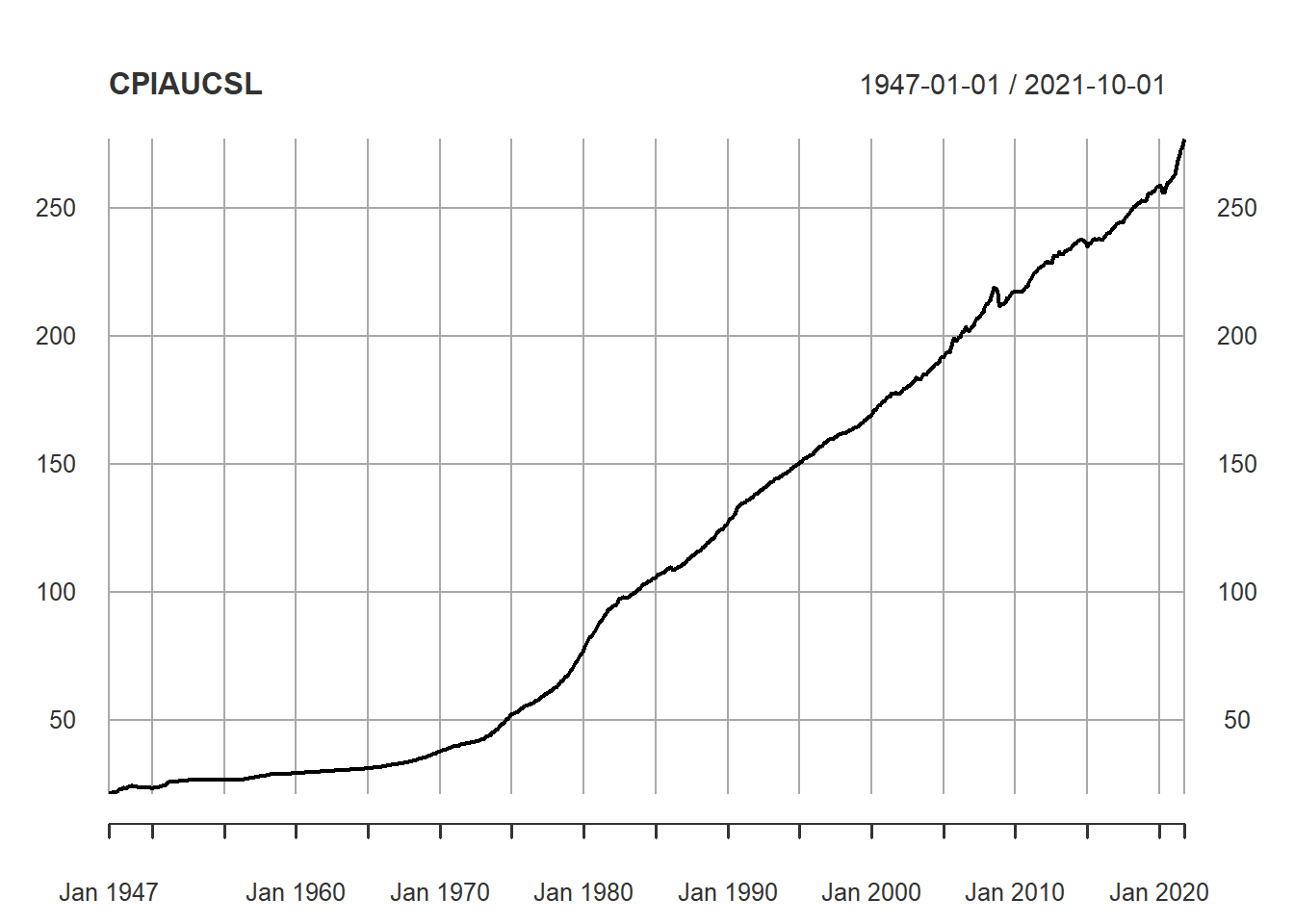

library(quantmod)## Loading required package: xts## Loading required package: zoo##

## Attaching package: 'zoo'## The following objects are masked from 'package:base':

##

## as.Date, as.Date.numeric## Loading required package: TTR## Registered S3 method overwritten by 'quantmod':

## method from

## as.zoo.data.frame zoo## Version 0.4-0 included new data defaults. See ?getSymbols.getSymbols("CPIAUCSL", auto.assign = TRUE, src = "FRED")## 'getSymbols' currently uses auto.assign=TRUE by default, but will

## use auto.assign=FALSE in 0.5-0. You will still be able to use

## 'loadSymbols' to automatically load data. getOption("getSymbols.env")

## and getOption("getSymbols.auto.assign") will still be checked for

## alternate defaults.

##

## This message is shown once per session and may be disabled by setting

## options("getSymbols.warning4.0"=FALSE). See ?getSymbols for details.## [1] "CPIAUCSL"getSymbols("USSTHPI", auto.assign = TRUE, src = "FRED")## [1] "USSTHPI"CPI <- read.csv("data/CPIAUCSL.csv")

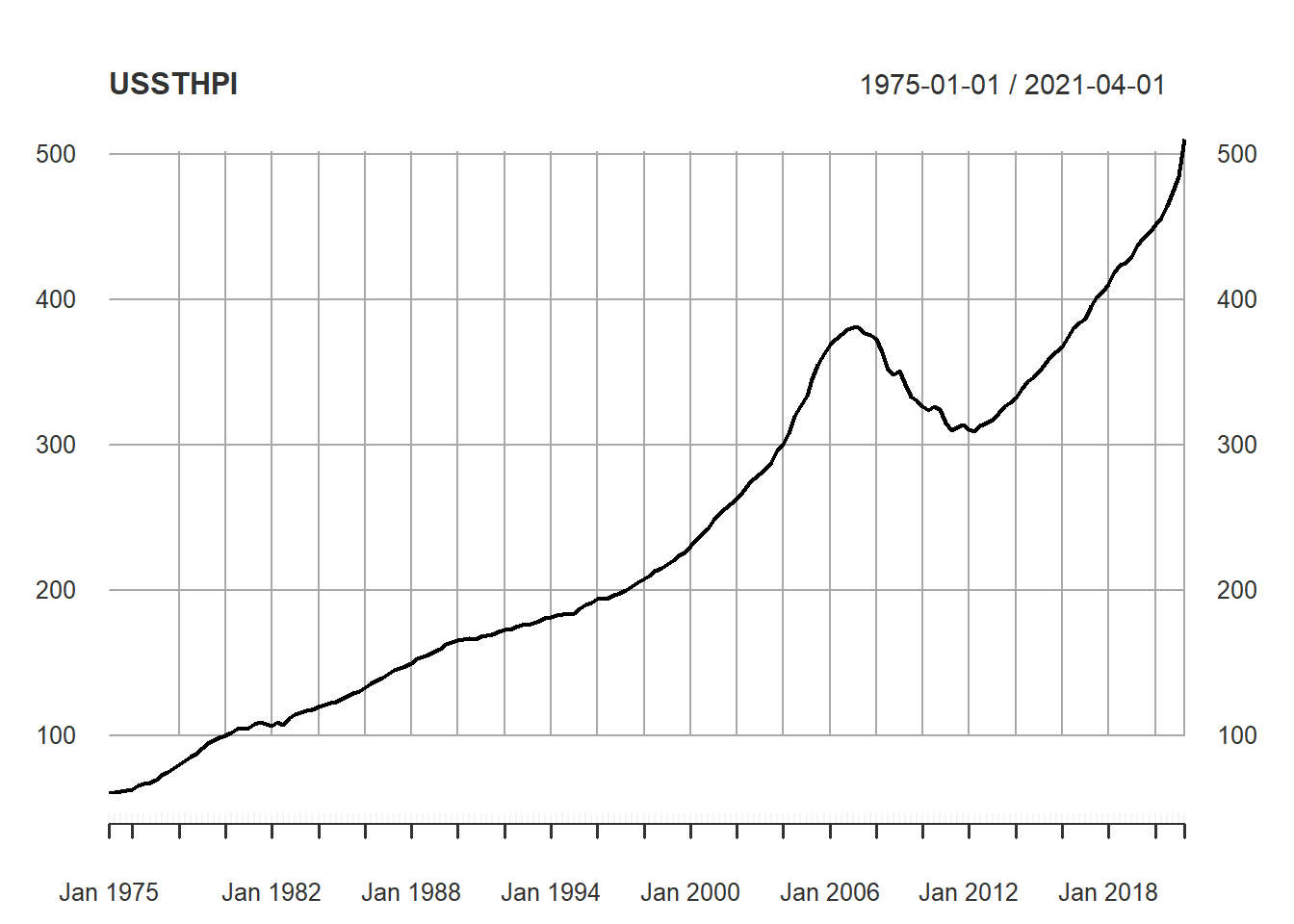

USHousePriceIndex <- read.csv("data/USSTHPI.csv")

plot(CPIAUCSL)

plot(USSTHPI)